The Effects of Rising Student Costs in Higher Education

Evidence from Public Institutions in Virginia

-

Table of Contents

- Acknowledgements

- Section 1: Purpose and Overview

- Section 2: Funding Trends

- Section 3: Trends in Net Costs at Four-Year Institutions

- Section 4: Trends in Student Enrollment, Retention, and Graduation

- Section 5: Descriptive Analysis of the Impact of Rising Net Costs on Student Success

- Section 6: Causal Analysis – A Difference in Differences Quasi-Experiment

- Section 7: Reflections on the Future

- Appendix

- Section A.1: Data and Methodology

- Section A.2: Robustness Checks

- Section A.3: Additional Results

- Section A.4: Funding Trends, Net Costs, and Student Decisions at Two-Year Institutions

- Acknowledgements

- Section 1: Purpose and Overview

- Section 2: Funding Trends

- Section 3: Trends in Net Costs at Four-Year Institutions

- Section 4: Trends in Student Enrollment, Retention, and Graduation

- Section 5: Descriptive Analysis of the Impact of Rising Net Costs on Student Success

- Section 6: Causal Analysis – A Difference in Differences Quasi-Experiment

- Section 7: Reflections on the Future

- Appendix

- Section A.1: Data and Methodology

- Section A.2: Robustness Checks

- Section A.3: Additional Results

- Section A.4: Funding Trends, Net Costs, and Student Decisions at Two-Year Institutions

In Virginia and elsewhere, higher education faces an unstable future. Demographic, economic and technological changes are driving transformation in all that we do. Higher education – access to it, knowledge created and disseminated through it, and outcomes produced by it – will be the key to innovation and prosperity. At the same time, public higher education faces an unprecedentedly challenging landscape as it seeks to fulfill its public purposes and responsibilities. Its transformative potential for our nation is at risk.

The risk is most evident in the ever-increasing tuition our colleges and universities charge. Regardless of the reasons, higher prices mean fewer families can gain the education and training they need to grow and prosper in their communities. Traditionally-underserved students, as well as families from deeper into the middle class, find it difficult to afford a college education. State and federal financial aid is not meeting the growing need, and more students face higher debt levels. While enrollment in higher education is leveling off, if not declining, demand for completers of postsecondary credentials has never been higher. We ignore these divergences at our peril.

Acutely aware of these challenges and trends, the State Council of Higher Education for Virginia spent much of 2014 developing the next statewide strategic plan for Virginia higher education. Our plan’s goals are as unsurprising as they are daunting – affordable access, student success, innovative change and improvement, and economic and cultural prosperity. Here, too, higher education’s purposes and responsibilities are central, and how to achieve their fulfillment, regardless of funding, remains the issue.

Ithaka S+R entered this swirling environment with a set of promising questions: What has been the impact of tuition and fee increases on enrollment patterns, student access and graduation? What strategies might the Commonwealth take to ensure affordable access to high-quality institutions? The findings corroborate and expand on what SCHEV has observed in its studies on the erosion of public funding – namely, reduced public funding diminishes institutional capacity, and higher prices threaten broad access. On many levels, we do not deserve the breadth and quality of our colleges and universities.

Dick Spies and his colleagues have done a tremendous job of consolidating data from a variety of sources (including SCHEV’s notable research site, http://research.schev.edu/ ), analyzing these data in creative ways, and articulating on-target explanations and conclusions. It has been no small task, and the report’s potential to inform conversations on the purposes and responsibilities of public higher education – and more importantly, public higher education’s ability to fulfill them – is equally large.

The team at Ithaka S+R was thoughtful, flexible and gracious throughout this effort. Virginia and its system of public higher education could not have asked for a more committed, skillful partner in this analysis. The Commonwealth will benefit from this work, and I am certain other states will as well.

Peter Blake, SCHEV Director

Acknowledgements

This study was undertaken by Ithaka S+R in partnership with the State Council of Higher Education for Virginia (SCHEV) and with the support of The Andrew W. Mellon Foundation. It arises out of a concern that public higher education, especially since the Great Recession that began in 2007-08, has not been able to produce a sufficient number of college graduates to satisfy regional and national needs for a better educated workforce, nor to function effectively as an accessible and affordable vehicle for less advantaged citizens to achieve economic and social mobility. In our view, Virginia represents an ideal setting to determine the extent to which this concern is supported by the evidence and, if so, what options are available for both the public institutions and the states that support them to do a better job of meeting these public responsibilities.

We are grateful to the Board and staff of SCHEV for their commitment to this project and for their willingness to assemble the very large database that we used to analyze these questions.[1] We are also grateful to The Andrew W. Mellon Foundation for its support for this project. Finally, we acknowledge with appreciation the many contributions of our colleagues at Ithaka S+R.[2]

Section 1: Purpose and Overview

Our Study

This study documents funding shifts for public higher education following the Great Recession and analyzes how different groups of institutions in Virginia have responded to those shifts. Our hypothesis is that the shift from a funding model largely supported by state appropriations to one primarily dependent on tuition revenue has made it more difficult for young people to pursue, and ultimately secure, a college degree at public institutions in Virginia. Moreover, to the extent that need-based financial aid programs in those institutions have not kept pace with rising student charges, we posit that students who come from economically disadvantaged backgrounds have been disproportionately affected. We chose to study Virginia because of the interest of the leadership of the State Council of Higher Education for Virginia (SCHEV) in better understanding these issues, the very rich database that SCHEV has built over time, and the similarities that its challenges hold to those of other states. We employ a micro-level dataset from SCHEV that contains observations covering more than 1.4 million students who enrolled in a public institution in Virginia between the 1997-98 and 2012-13 academic years.[3] The very high degree of completeness and accuracy of the data used in this study – which encompass the entirety (and not just a sample) of the public college-enrolling population in Virginia – sets it apart from previous studies that have analyzed these issues, and provides a powerful empirical foundation upon which to estimate the relationships and draw the conclusions that we describe in this report.

As this report will detail, we found significant evidence that public higher education in Virginia is falling well short in its efforts to meet broader national goals of increasing overall educational attainment and narrowing the gaps that exist in educational levels between students from different socioeconomic backgrounds. Declining state appropriations and increasing reliance on tuition revenue have substantially increased the cost of public higher education to Virginia students, and the trend has accelerated since the Great Recession that began in 2007. Rising costs have deterred students from remaining in college and completing their degrees, and the lowest-income students have been hit the hardest. These results are particularly discouraging given that public higher education as a whole in Virginia – as in most states – was already falling well short of achieving these goals even before the latest declines in state support and increases in tuition came into effect. This study measures the degree to which these trends have worsened since the Great Recession and raises the alarm about what the future will be like if nothing is done to turn the present situation around.

Public Higher Education: Mission and Challenges

The central mission of public higher education in this country is to educate and prepare young adults to assume productive roles in a modern workforce, contribute to our national and regional economic competitiveness, strengthen our communities and nation as educated and caring citizens, and live enriching lives. As part of the special American dream of “equal opportunity for all,” public higher education also plays a critical role in seeking to eliminate, or at least narrow, gaps in opportunity between young people born into different socioeconomic circumstances. As far back as the Morrill Act of 1862 (which created our system of state-supported land grant universities), these goals have been the hallmark of American public higher education.[4]

In recent years, the first goal of increasing the number of college graduates in the U.S. has received wide attention from various policymakers and stakeholders. Most notably, in 2009, President Obama proposed that by 2020 America would once again have the highest proportion of college graduates in the world.[5] To reach this goal, the U.S. would need more than 65% of individuals between the ages 25 and 34 to possess a college degree.[6] Various private foundations (including Gates and Lumina) have established similar targets in recent years to challenge colleges and universities to respond accordingly.[7] While the specific goals and timetables vary, the need for more better-educated young people to enter and build our workforce – and, by extension, our citizenry – has never been clearer.

The second goal of reducing the opportunity gap between students from different socioeconomic backgrounds is also critical, both in itself and as a means to increase overall educational attainment in our society. Starting with the GI Bill of the post-World War II era and the original Higher Education Act of 1965, the goal of equalizing opportunity has received broad public endorsement at the national, state, and local levels. Public colleges and universities are critically important in that effort, as they educate a large majority of low- and middle-income students. Furthermore, President Obama’s recent call to make community college tuition-free is aimed directly at shrinking the opportunity gap by removing some of the cost barriers to higher education access and degree attainment.[8]

National Context

Notwithstanding this high-level attention, progress on both of these goals remains discouragingly slow. Nationally, only 42% of 24-35 year olds had a post-secondary degree as of 2012.[9] While the enrollment rate of 18-24 year olds in postsecondary education modestly improved from 39% to 42% between 2007 and 2011, this rate dropped to 41% in 2012.[10] More importantly, current enrollment rates are much too low to produce a significant change in the overall number of degree holders, and too many students who do enroll at a post-secondary institution leave without a degree.[11] Finally, a student from an upper-income family where at least one parent has a college degree is almost eight times more likely to get a college degree than a student from a low-income family where neither of the parents has a college degree – dramatic proof of a very large gap between the educational opportunities available for different socioeconomic groups.[12]

Affordability and access to higher education are challenges for most public institutions, and states and institutions wrestle annually with the specific challenges associated with setting tuition and fees and providing adequate funding for need-based financial aid programs. In 2012, for the first time since the turn of the century, tuition as a share of total revenue surpassed the share associated with state funding for public institutions nationwide.[13] At the same time, states and institutions are trying to do more to improve student outcomes and reduce the gaps between less advantaged students and their more well-to-do counterparts.

Unfortunately, despite significant efforts on the part of many state and institutional leaders, not enough progress has been made to meet the goals of increasing the number of college graduates and decreasing the opportunity gap between students from different socioeconomic backgrounds. Significant reductions in state appropriations for higher education have made it difficult to support even current enrollment levels, with 49 states spending less per undergraduate in 2011-2012 than before the Great Recession, and 28 states actually decreasing per-student funding by more than 25 percent since 2008.[14] In particular, the Great Recession that officially began in 2007 weakened not only state budgets but also the priority given to higher education within those budgets.[15] Colleges and universities historically dependent on public support began increasingly to rely on tuition and other student charges for the resources needed to support their programs, with tuition charges at public four-year institutions increasing by a national average of 20% between 2008 and 2012.[16] Concurrently, stagnating family incomes have resulted in tuition as a fraction of family income growing by 3.5% from 2008 to 2012.[17]

Similar financial patterns are evident in Virginia, which currently provides only about half as much support per student at public institutions as it did in 2001.[18] Virginia ranked 35th nationwide in state funding per FTE (full-time equivalent) as of 2011-2012, and it has seen average tuition as a share of family income at public four-year institutions rise by 3.9% (slightly above the national average) from 2008 to 2012.[19] Thus, in terms of these financial challenges, Virginia seems to be a microcosm of the public higher education scene in the country. Given that Virginia is also an economically and demographically diverse state with characteristics similar to the national average, we believe that the conclusions drawn from our analysis of financial trends and student outcomes in Virginia apply broadly to many other states and public institutions.[20]

Summary of the Results

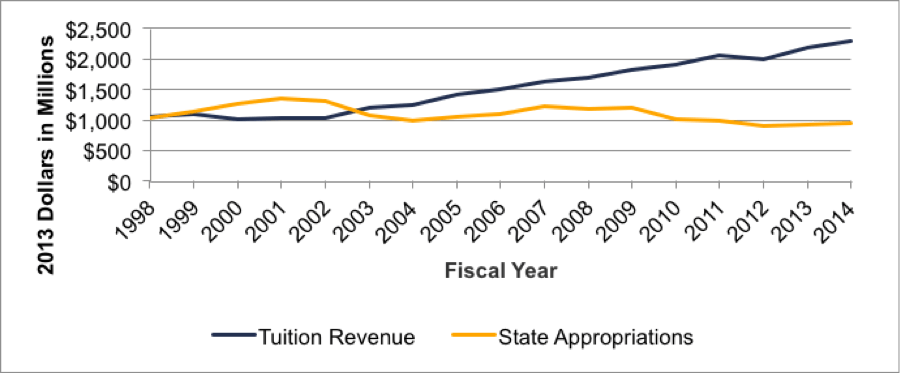

Over the past decade and a half, there has been a dramatic shift in Virginia higher education financing away from state appropriations and toward tuition.

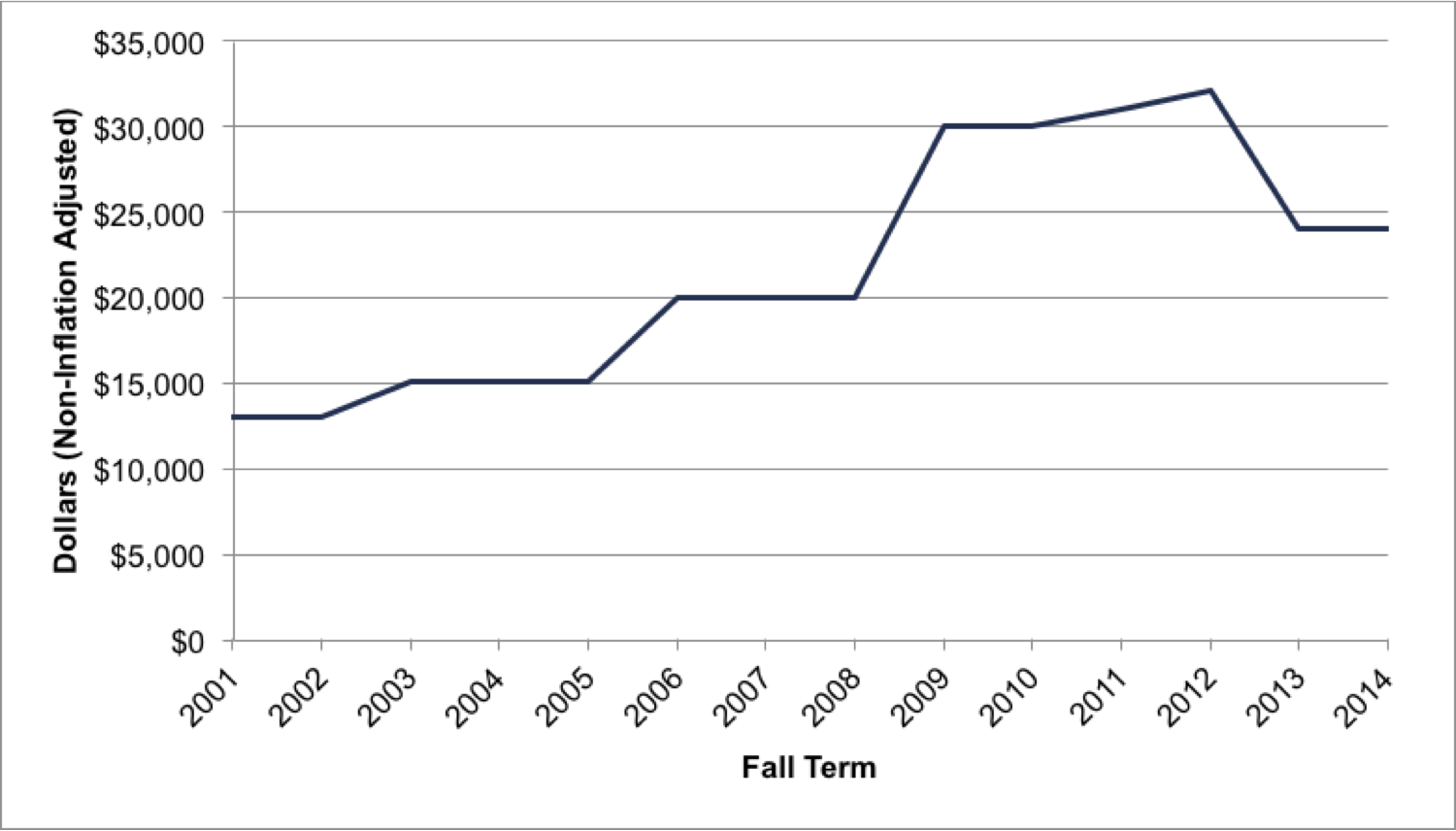

Over the past decade and a half, there has been a dramatic shift in Virginia higher education financing away from state appropriations and toward tuition. Inflation-adjusted state appropriations in Virginia declined by 30% between fiscal years 2001 and 2014 (Figure 1.1). As a result, nearly every public institution has had to become significantly more dependent on tuition revenue in order to pay for the resources they need, ranging from faculty salaries to financial aid (see Section 2).

While decreases in state funding are not unprecedented, there are several factors that make the significant declines since the beginning of the Great Recession in 2007 particularly concerning; these include the severity of the most recent recession, the proximity and compounding nature of the last two recessions (in 2001 and 2007), and the large increases in enrollment that have placed additional pressures on state resources. Based on the state’s recent budgets, it does not appear likely that this situation will be significantly repaired or reversed in the foreseeable future.

Figure 1.1. Total Revenue from Tuition and State Appropriations

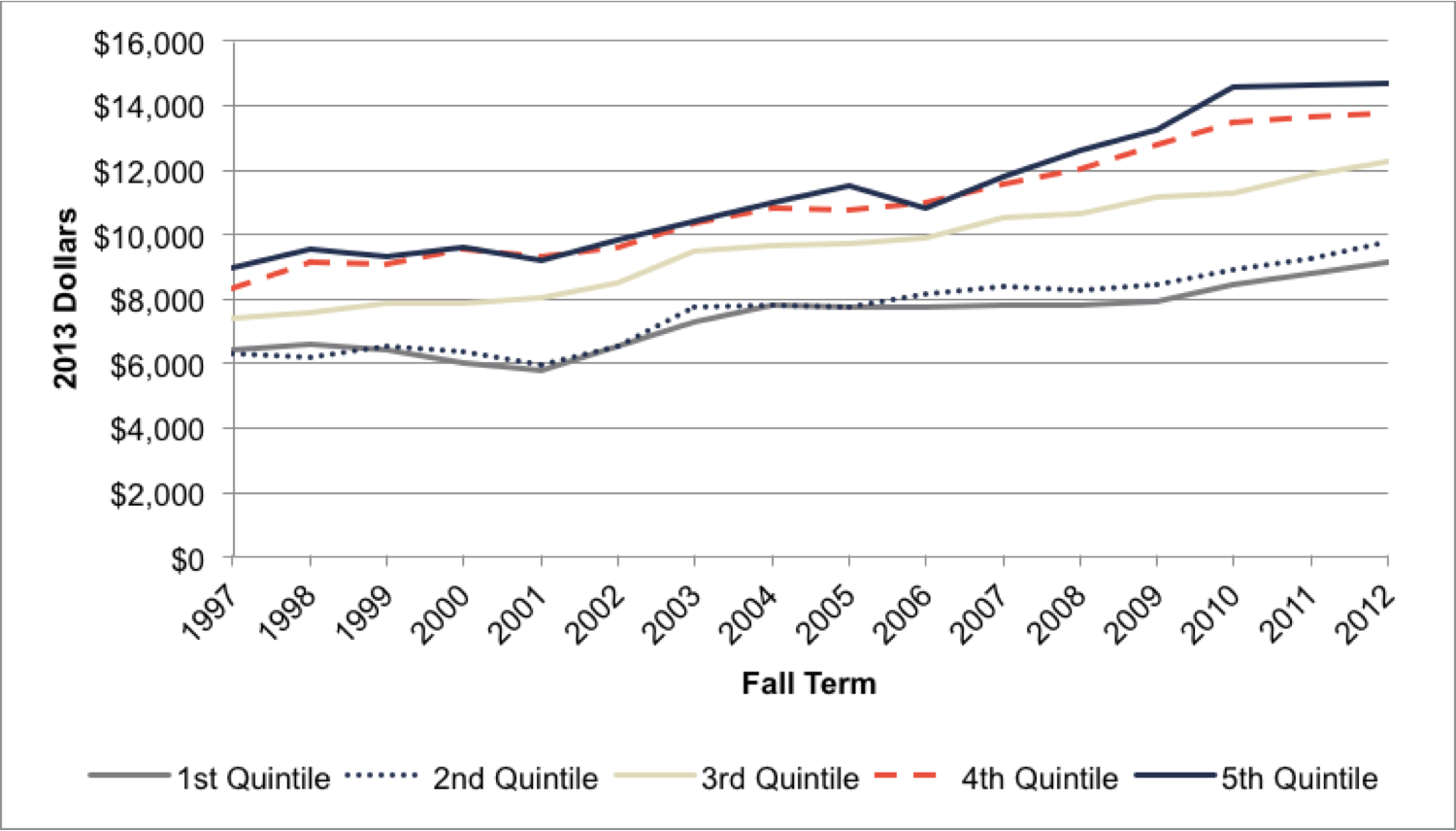

Different institutions within Virginia have taken somewhat different approaches in responding to the challenges represented by the decline in public funding, but tuition levels have nevertheless gone up significantly for all institutions, while financial aid programs have generally not been able to keep pace. The key measure of student costs used in this study is inflation-adjusted net costs, defined as the difference between a student’s estimated cost of attendance and the total amount of gift aid received for an academic year. Based on our analysis of data for 1,450,321 students who enrolled in a Virginia public institution between the 1997-1998 and 2012-2013 academic years, net costs at four-year public institutions have increased at rates well above inflation for in-state, full-time, first-time freshmen from most socioeconomic groups since 1997 (see Section 3).[21] Furthermore, these increases have accelerated since the recession began in 2007, as many institutions expanded student charges and/or cut back on need-based financial aid.

Between 2007 and 2012, net costs grew 3.5% per year above inflation for the lowest income quintile, compared to lower rates for the other income groups.

It is especially worrying that, since 2007, net costs have grown fastest for the lowest income students (Table 1.1). Between 2007 and 2012, net costs grew 3.5% per year above inflation for the lowest income quintile, compared to lower rates for the other income groups.[22] This represents a significant change from the pattern prior to 2007, when net costs grew fastest for the highest-income students and stayed almost flat for the poorest students.

Table 1.1. Average Annual Growth Rates in Net Costs at Four-Year Institutions by Income Quintile

| 1st Quintile | 3rd Quintile | 5th Quintile | |

|---|---|---|---|

| 1997-2007 | -0.2% | 1.9% | 1.8% |

| 2007-2012 | 3.5% | 3.2% | 2.6% |

| Total (1997-2012) | 1.0% | 2.3% | 2.1% |

…fewer than 25% of the lowest-income Virginia students who enrolled in a public college or university in Virginia went to a four-year institution…more than 90% of students in the highest-income quintile who enrolled in a public postsecondary institution in Virginia did so at a four-year institution.

At the same time that net costs have grown fastest for students from the lowest-income groups, we observed some troubling patterns in enrollment and outcomes for these students (see Section 4). First, fewer than 25% of the lowest-income Virginia students who enrolled in a public college or university in Virginia went to a four-year institution, whereas more than 90% of students in the highest-income quintile who enrolled in a public postsecondary institution in Virginia did so at a four-year institution. While overall enrollment numbers have risen for most institutions since 2001, there has been essentially no progress since 2007 in shrinking this very large “enrollment gap” among students from different income backgrounds. This is particularly troubling since only 5% of students who enroll full-time in a two-year college earn an associate’s degree within two years, and only 2% earn a bachelor’s degree (through transferring to a four-year institution) within four years.[23]

Second, even those students from lower-income families who do enroll in four-year institutions are less likely than their higher-income peers to remain enrolled, persist through, and graduate from those institutions, a gap that has endured throughout this entire time period. Since the 1990s, the first-year retention rate for students in the 1st income quintile has consistently been about 11 percentage points lower than for their peers in the 5th income quintile.

Our analysis of the patterns of student achievement makes clear that increases in net costs have a statistically significant, negative effect on student success; the effect is largest for the poorest students.

Finally, our analysis of the patterns of student achievement makes clear that increases in net costs have a statistically significant, negative effect on student success, and that the effect is largest for the poorest students (see Section 6).[24] In our most robust analysis, a difference-in-differences evaluation of an exogenous change in expected family contribution (EFC) allows us to directly test the causal impact of a change in net costs. Here, we find that a federal policy change that increased the income threshold for students to qualify for zero expected family contribution (which was associated with an average decrease in net costs of $400 per year) results in a 5.9 percentage point increase in the probability that a low-income student will persist after his or her first year (see Section 6). We also examined the relationship between net costs and student success using ordinary least squares specifications (see Section 5). Although the effects of net costs estimated using these techniques are smaller and do not allow a causal inference, we still found statistically significant inverse relationships between net costs and outcomes in all specifications we examined – with the magnitudes largest for students from the lowest EFC quartile. Analysis using other outcome measures, including the number of credits completed, progress towards a four-year degree, and the likelihood of graduating in four years, tells the same story. While there have not yet been significant absolute declines in retention and graduation rates in Virginia, our findings strongly suggest that the disproportionately large increases in net costs for low-income students will exacerbate disparities that already exist among different groups of students and eventually affect overall enrollment and success rates.

Section 2: Funding Trends

Public colleges and universities in Virginia are facing considerable financial challenges from significant declines in state appropriations. These challenges have been exacerbated in recent years by a global recession that has simultaneously reduced state revenues and diminished family incomes.[25] While cuts in state funding are not unprecedented, two factors make the current situation different and, as a result, significantly more problematic. First, the nature and depth of the latest recession led the state to reduce funding per student to historically low levels since 2007, with few signs that funding will be restored in the near future. Second, the strategies that have allowed institutions to successfully navigate funding cuts in the past – including increasing student charges and/or enrollment – are unlikely to be as successful moving forward. While some institutions have been better able to weather the recent budget cuts than others, and may have some capacity to deal with further cuts going forward, the evidence suggests that the ability of most institutions to serve their respective missions within current budget constraints is very much at risk.

In this section, we describe trends in state funding between the 1993 and 2014 fiscal years.[26] We rely on data from SCHEV (most of which are publicly available on its website) and the Delta Cost Project Database (which utilizes IPEDS data) for institution- and state-level data on state and financial measures and school characteristics. All dollar values have been adjusted for inflation and are reported in 2013 dollars. All reported years in this section refer to the fiscal year (e.g., the 2013-2014 academic year is referred to as the 2014 fiscal year). Additional details concerning the data and our methods for analyzing them are available in Section A.1 of the Appendix.

Decline in State Support

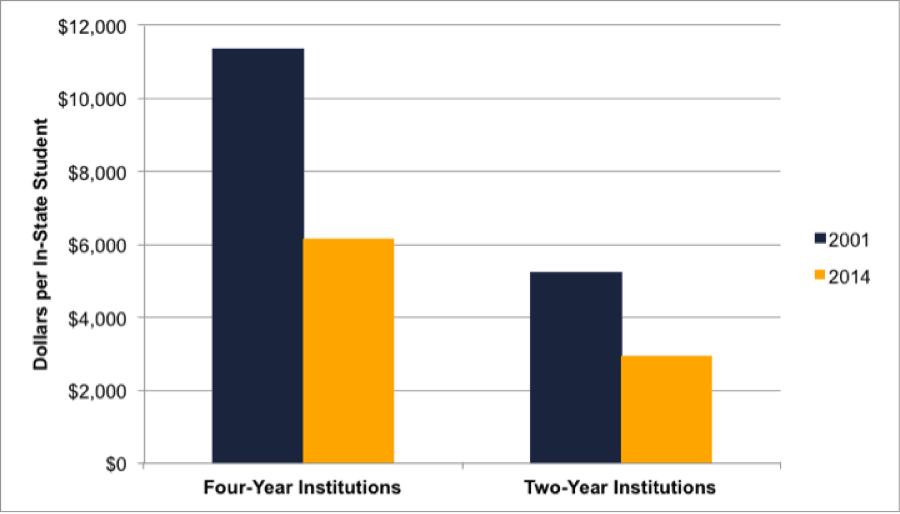

Over the last two decades, state appropriations per undergraduate student have fallen across all public institutions in Virginia, with the reductions over the past ten years having been particularly steep and applicable to every public institution, four-year and two-year alike. Between fiscal years 2001 and 2014, state funding per in-state student declined by 46% and 43% at four-year and two-year institutions, respectively (Figure 2.1).[27] Compared to reductions in state funding that have occurred in the past, the unique severity of these cuts will likely result in more serious and longer-lasting impacts.

Figure 2.1. State Appropriations per In-State Student

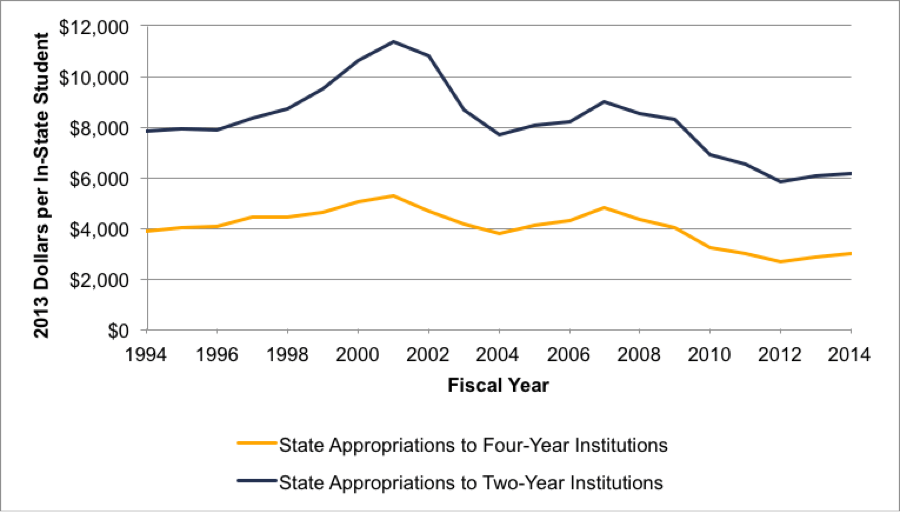

In Virginia, as in most states, state funding for higher education is closely correlated with the strength – and volatility – of the economy. As Figure 2.2 illustrates, cuts in state funding typically take place in the immediate aftermath of a recession. Figure 2.2 shows low points in state funding in the early 1990s (which followed the recession of 1990) and immediately following the recession of 2001, along with the very large cut in funding that resulted from the Great Recession that began in 2007. In the first two cases, we experienced significant upturns in funding as the economy recovered, especially during the prolonged economic expansion of the mid- and late-1990s. The current recession – the Great Recession – appears to be different in important ways, however, and there is reason for concern about current and future levels of state funding even as the state and the nation slowly recover.

Figure 2.2.

The first reason for concern is that the severity of the Great Recession that began in 2007, and the very slow global recovery that has followed, make it unlikely that state funding for higher education will recover as quickly as it did following the 1990 and 2001 recessions. While state appropriations have historically increased as the economy recovered from recessions, the current post-recession economy is far weaker than the economy that followed the 1990 recession. As Figure 2.2 indicates, the lowest levels of state funding resulting from the 1990 recession (which occurred between 1993 and 1995) were still nearly $1,000 per student higher than the level in 2013. Even as Virginia’s economy begins to recover, there are few signs that this recovery will extend to public higher education in the near future. To the contrary, public colleges and universities are facing the strong possibility of continuing reductions in funding.[28]

Furthermore, the proximity of the last two recessions has compounded their impact on institutional finances, leading to greater total cuts in public funding. While the cuts from the 1990 recession were actually larger (in absolute terms) than those from the 2001 or 2007 recessions, the economy had almost twice as long to recover between 1990 and 2001 as it did between 2001 and 2008. As a result, appropriations per in-state student after the 2001 recession were still 24% lower than their peak levels upon the onset of the 2007 recession. Combining the effects of the two recessions, we saw overall reductions that were larger than those previously experienced and from which there was less time to recover. The result was a decline in funding between 2001 and 2014 that was much larger than the decline after the 1990 recession.[29]

Finally, large increases in enrollment (particularly since the Great Recession) have placed additional pressures on state resources, driving down funding on a per-student basis and making it less likely that these levels will return to their pre-recession heights. Between 1994 and 2014, four-year and two-year institutions saw a 35% growth in in-state enrollment,[30] meaning that Virginia would have had to substantially increase funding for higher education in order to maintain per student levels of support.[31] To be more specific, the state would have had to invest an additional $1.1 billion per year in higher education (equivalent to an 86% increase from its actual level in 2014) to reinstate per-student funding back to its 2001 level. Instead, rather than becoming a funding priority, appropriations to higher education have actually gone down as a fraction of the total state budget, with general fund support dedicated to higher education declining from 14% of the state budget to 11% between 1993 and 2010.[32]

Institutional Responses to Funding Cuts

While all public institutions in Virginia have experienced declines in state support, they have responded in varying ways. In particular, we noticed significant distinctions between two-year and four-year institutions, as well as among different groups of four-year schools, in terms of their abilities to offset declines in state funding with alternative sources of revenue. The four-year institutions that appear less able to generate new revenue and are therefore more dependent on state funding are referred to in this study as “Higher Dependence on the State” (HDS) institutions. These institutions include: University of Mary Washington, Virginia State University, Christopher Newport University, Longwood University, Old Dominion University, University of Virginia’s College at Wise, Radford University, and Norfolk State University. The four-year institutions that have greater capacities to generate revenue from alternative sources and are therefore less dependent on state funding are referred to as “Lower Dependence on the State” (LDS) institutions.[33] These include: University of Virginia, College of William & Mary, George Mason University, Virginia Military Institute, Virginia Commonwealth University, James Madison University, and Virginia Tech. In this subsection, we document the strategies adopted by public institutions as a whole and how they differ among these groups of institutions.

State appropriations and tuition revenues have historically constituted the majority of total revenues for most of Virginia’s public institutions of higher education. However, recent declines in public support have forced all of Virginia’s public institutions to become increasingly reliant on tuition revenue in order to balance their budgets. As a result, nearly every institution has raised both its in-state and out-of-state tuition rates, although the magnitude of these increases has varied by institutional type. Institutions have also increased enrollment as a way of increasing tuition revenue, although it is likely that this only increases aggregate revenue from net tuition while actually leading to reductions in revenue per student.[34] We examine below in more detail how the three types of institutions – LDS, HDS and two-year – responded to declines in state support.

Among LDS institutions, state funding as a share of total revenue dropped from 43% to 23% between 2001 and 2010. Although LDS institutions are able to bring in about 25% of their revenue from sources other than state funding and tuition revenue, they have still seen net tuition revenue as a percent of total revenue increase from 27% to 41% during this time period.[35] Indeed, increases in tuition rates at LDS schools have occurred for all students, with in-state and out-of-state charges increasing by 107% and 81%, respectively, between 2001 and 2014 (Figures 2.3 and 2.4). Compared to HDS institutions, LDS institutions appear to be better able to generate tuition revenue from both resident and non-resident students, with the absolute increase in in-state tuition among LDS institutions approximately 30% greater than that for HDS schools. In addition, despite the large increases in out-of-state tuition charges, LDS institutions were able to increase out-of-state enrollment by 57% between 2001 and 2014. As we will discuss in more detail below, these two strategies have allowed LDS institutions to offset a greater portion of the state’s funding cuts.

Figure 2.3. Average In-State Tuition and Fee Charges

Figure 2.4. Average Out-of-State Tuition and Fee Charges

In contrast with their LDS peers, HDS institutions relied much more on increases in in-state enrollment (which rose by 38% between 2001 and 2014) to grow total tuition revenue. Even though HDS institutions also increased in-state and out-of-state tuition rates appreciably between 2001 and 2014 (by 105% and 61%, respectively), these increases were significantly smaller than those observed by LDS institutions. As a result of these strategies and a decline in public support, the share of total revenue for HDS institutions that came from state funding dropped substantially between 2001 and 2010 (from 56% to 47%). By and large, two-year institutions have also responded to financial challenges in similar ways to the four-year HDS schools – albeit with an even greater reliance on increasing in-state tuition rates and enrollment.

In the midst of these budgetary pressures, four-year institutions as a whole have made considerable investments in financial aid since 2001, with in-state institutional aid as a share of in-state gross tuition rising from 5.9% in 2001 to 13.0% in 2013. However, because this share was very small to start with, the rates of increase would have had to be significantly larger to support more than a small handful of students. Moreover, recent declines in federal and state aid as a fraction of gross tuition have resulted in total aid awarded to in-state students as a share of in-state gross tuition decreasing from 71.1% in 2001 to 69.6% in 2013. In other words, the decreases in the shares associated with state and federal aid have more than canceled out the increases in institutional aid. We will have more to say about the connections between tuition and financial aid in the next section when we address how these institutional decisions affect the net costs that students confront.

Impact on Overall Institutional Financial Structure and Health

Taken together, the data suggest that the three groups of institutions – LDS, HDS, and two-year – relied on somewhat different mixes of strategies in order to increase revenue from net tuition (Table 2.1). LDS institutions relied heavily on higher in-state charges and increases in out-of-state tuition charges and enrollment. HDS institutions – and, to an even larger extent, two-year institutions – instituted increases in tuition charges but also implemented large increases in in-state enrollment. These different approaches have resulted in different implications for institutional finances.

Table 2.1 Changes in Institutional Finances and Enrollment by Institutional Groupings

| Average In-State Tuition 2001-2014 | Average Out-of-State Tuition 2001-2014 | Total In-State Enrollment 2001-2014 | Total Out-of-State Enrollment 2001-2014 | Average Institutional Gift Aid 2001-2014 |

||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Percentage change from 2001 | Average Tuition Charge: 2014 | Percentage change from 2001 | Average Tuition Charge: 2014 | Percentage change from 2001 | Total Enrollment: 2014 | Percentage change from 2001 | Total Enrollment: 2014 | Percentage change from 2001 | Average Institutional Gift Aid: 2014 | |

| LDS | 107% | $11,695 | 81% | $31,433 | 26% | 86,706 | 32% | 25,437 | 49% | $10,336,165 |

| HDS | 105% | $9,070 | 61% | $21,598 | 38% | 50,639 | -25% | 5,457 | 63% | $6,718,312 |

| Two- Year | 120%* | $4,088* | 56%* | $11,934* | 40% | 181,660 | 8% | 8,868 | 583% | $778,241 |

*Tuition data for two-year institutions are only available up to 2013.

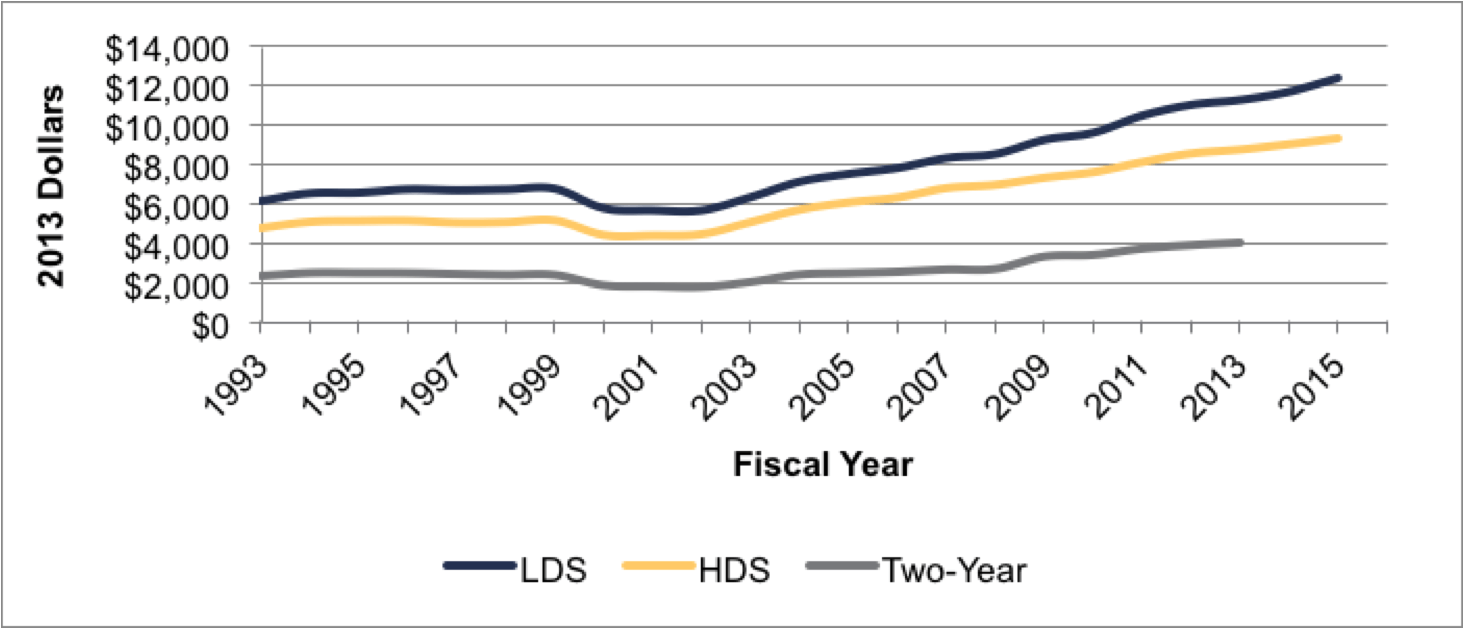

At the risk of underestimating the challenges involved for all institutions, it appears that LDS institutions have been generally successful at offsetting declines in state support, including the large reductions experienced in recent years. Between 2008 and 2014, for example, LDS institutions managed to produce an average increase of 5% per year in combined revenue from tuition and state appropriations per FTE student primarily due to their ability to bring in significant revenue from out-of-state students and maintain high levels of in-state tuition (Figure 2.5). These factors allowed LDS institutions to generate sufficient revenue from tuition to more than offset the loss of state funding without having to resort to large increases in in-state enrollment.[36]

Figure 2.5. Combined Revenue from Tuition and State Appropriations per FTE Student

HDS institutions, on the other hand, have had much more difficulty maintaining per-student revenue levels. As Figure 2.5 shows, combined revenue from tuition and state appropriations per FTE student declined by an average of 9% between 2008 and 2014, which can be attributed to the rapid expansion of in-state enrollment without comparable increases in out-of-state enrollment or other means of support.

Finally, two-year institutions have been able to offset much of the decline in public funding. In addition to substantial growth in in-state enrollment, they generated a significant amount of revenue by considerably increasing in-state tuition charges. In total, combined tuition and state appropriations revenue per FTE student decreased by an average of only 2% between 2008 and 2014, a result of shifting the cost burden onto in-state students. While perhaps necessary financially, this is worrisome since in-state students are arguably the least able to deal with an increase in charges and most of these institutions have little to no aid to provide for these students.[37]

Are These Strategies Sustainable?

In the face of current financial challenges, public institutions have largely relied on strategies used in the past. While Virginia’s public institutions have historically been able to successfully offset funding declines through increasing tuition and enrollment, the severity of recent challenges casts doubt on the ability of many of them to keep following these paths. More specifically, tuition charges may be reaching their market limit at many of these institutions, and further increases could both adversely impact institutional finances and endanger the goals of ensuring quality and broad access for students across the state. HDS institutions, in particular, appear to have reached – or at least come close to – this limit, as they were unable to increase tuition charges enough to offset the most recent funding cuts and have thereby seen declines in total revenue per student. And while LDS and two-year institutions have so far been able to institute tuition increases large enough to replace declining state support without a significant market pushback, student demand may not persist if charges continue to rise at such rapid rates.

Indeed, such declines may already be manifesting themselves across the two-year colleges. Table 2.2 illustrates how declines in enrollment have become apparent in two-year institutions over the last few years. If such declines are a sign of price outstripping demand, then four-year and two-year institutions alike may have difficulty in sustaining enrollment and tuition revenues in the future.

Table 2.2. Enrollment and Tuition Changes at Two-Year Institutions

| Two-Year Institutions | 2008-2010 | 2010-2011 | 2011-2012 | 2012-2013 |

|---|---|---|---|---|

| Number of institutions with decreased enrollment (out of 24) | 0 | 6 | 12 | 20 |

| Average percentage change in enrollment (annual) | 7% | 3% | -1% | -4% |

| Average tuition increase | 13% | 9% | 5% | 3% |

Even if the current tuition levels are sustainable from a purely financial perspective, the current reliance on increasing tuition revenue may limit the ability of many institutions to serve their respective missions. In particular, these financial strains may force institutions to choose between sacrificing either access or quality (or some combination of both), particularly for low- and middle-income students. On the one hand, if revenue from tuition increases goes towards filling gaps in the budget left by the declines in state support rather than funding financial aid, the majority of students may see real and substantial increases in the net costs they are expected to pay. On the other hand, if institutions choose to keep tuition low and financial aid high as a way of preserving access for as many students as possible, they will have to think carefully about how to reduce expenditures without sacrificing the quality of the education they provide. Unfortunately, the current funding situation has brought Virginia public higher education to the point of having to make these difficult kinds of choices.[38]

Section 3: Trends in Net Costs at Four-Year Institutions

We now examine how the changes in the institutional- and state-level financial trends have led to changes in the first-year net costs that students pay to attend a public institution of higher education in Virginia. We use a student-level dataset obtained from SCHEV that contains longitudinal background and financial data for 1,450,321 million students who entered a Virginia public institution of higher education between the 1997 and 2012 academic years.[39] For a more detailed description of the data and the methodology employed, see Section A.1 of the Appendix.

In this section, we look at in-state, first-time freshmen entering a Virginia public four-year institution on a full-time basis between the 1997 and 2012 academic years, concentrating especially on those who have entered since the beginning of the Great Recession in 2007. Minor adjustments to our sample (due to complications in the data) are described in the footnotes and in greater detail in the Appendix.[40] We focus primarily on how net costs have changed for poor and near-poor students, using the highest-income students as the main point of comparison. We define net cost as the difference between a student’s total budget for an academic year and the total amount of gift aid (including need-based grants and merit aid) received for that year.[41] All dollar values are adjusted for inflation and reported in 2013 dollars.

Trends in Average Net Costs

We chose to define our student cohorts based on state-wide income quintiles, designating poor, near-poor, and highest-income students as those who come from families with incomes in the 1st (lowest), 3rd (middle), and 5th (highest) income quintiles in Virginia, respectively.[42] Defining socioeconomic subgroups in this way allows us to categorize these groups based on objective characteristics of the state’s population. For a sense of what these quintiles look like, Table 3.1 breaks them down by their income ranges for 2012 and their median income levels within our sample of interest.[43]

Table 3.1. Family Income by Income Quintile (2013 Dollars)

| 2012 Income Range | Median for Sample | |

|---|---|---|

| 1st Quintile | $0 - $25,320 | $14,912 |

| 2nd Quintile | $25,321 - $49,795 | $39,526 |

| 3rd Quintile | $49,796 - $76,000 | $65,839 |

| 4th Quintile | $76,001 - $120,670 | $101,996 |

| 5th Quintile | $120,671+ | $165,890 |

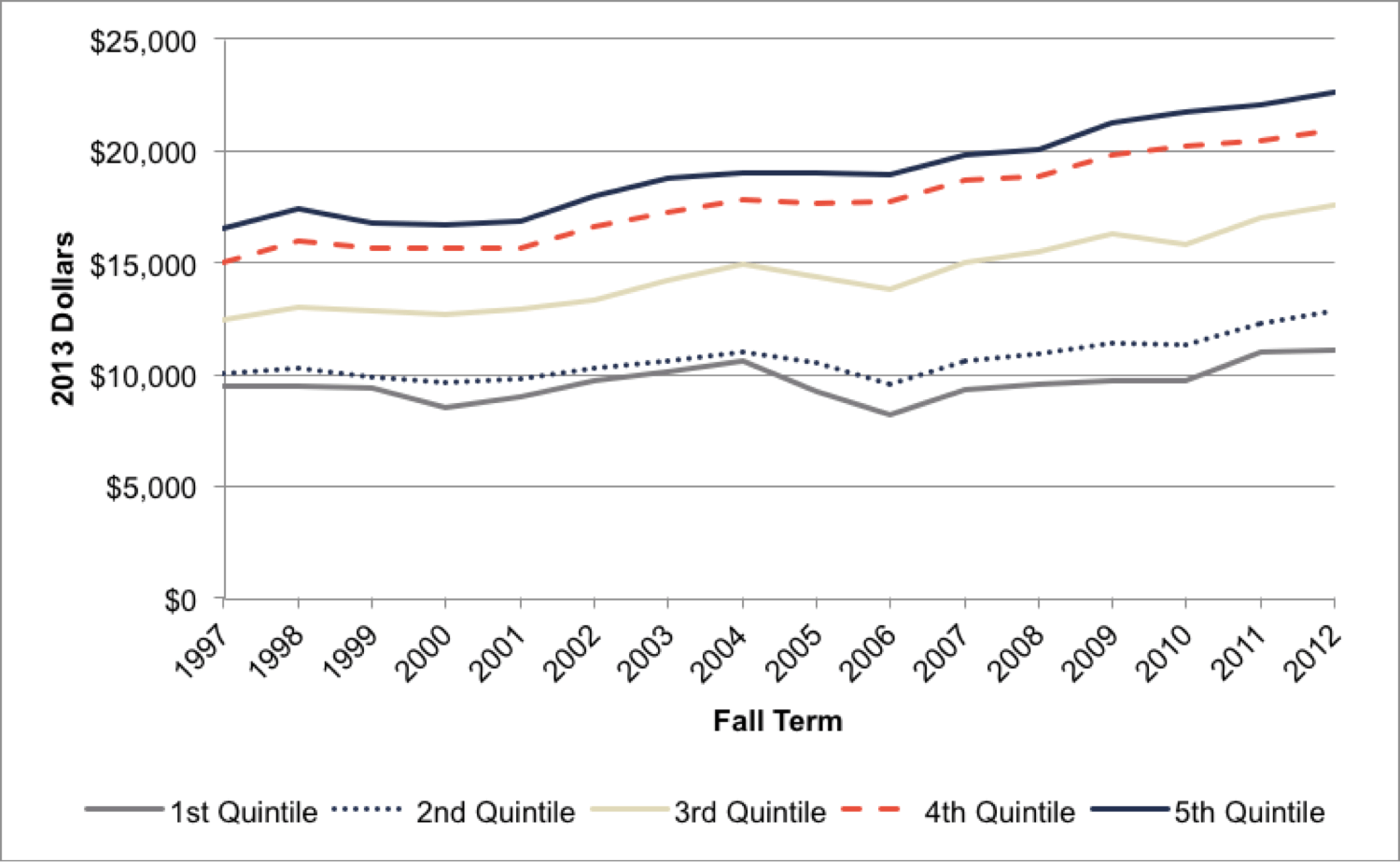

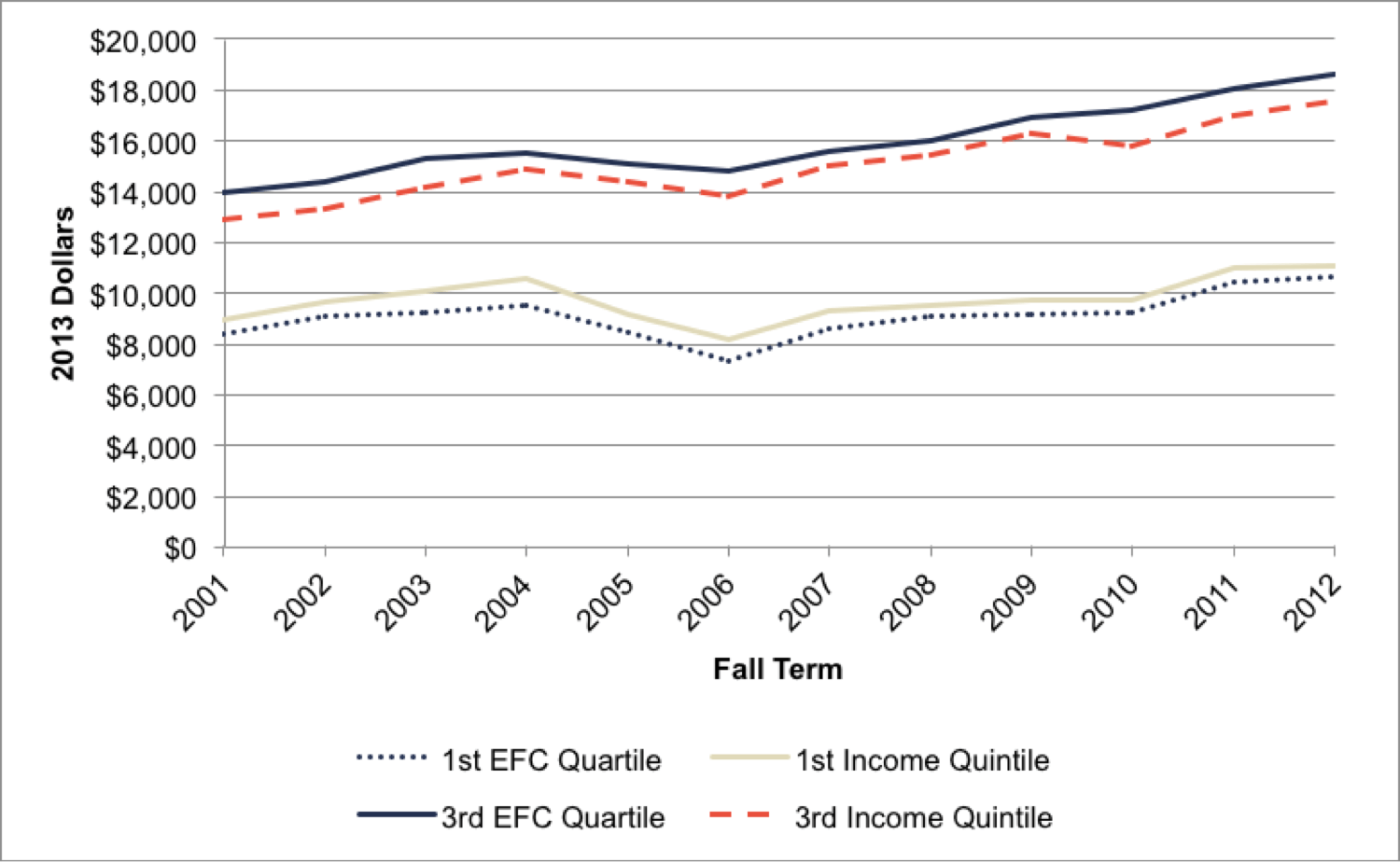

Figure 3.1 illustrates the trends in average net costs between 1997 and 2012 for each income quintile at public four-year institutions in Virginia. We observe that net costs have increased at rates above inflation for nearly every group between 1997 and 2012, with these increases accelerating and becoming more consistent since 2007.[44] Prior to 2007, the increase in net costs had been greatest – and most steady – for the near-poor and highest-income students, while net costs actually decreased slightly on an average annual basis for students in the lowest income quintile (Table 3.2).[45] However, after 2007, net costs grew fastest for the poorest students (at an average annual rate of 3.5%) and more slowly for the highest income students – a reversal of the pattern previously observed.

before 2007.[46] This recent growth in net costs for the poor – and, to a slightly lesser extent, the near-poor – was driven primarily by large increases in these costs from 2010 to 2011, when net costs grew at annual rates of 12.8% and 7.4% for the poor and near-poor, respectively. Moreover, the compounding effect of the Great Recession can be discerned most clearly for near-poor students, for whom net costs in 2006 began to increase even before they were able to fully recover to pre-recessionary levels following the effects of the 2001 recession.

Figure 3.1. Changes in Net Costs over Time

Table 3.2. Annual Rates of Change in Net Costs by Income Quintile

| Poor (1st Quintile) | Near-Poor (3rd Quintile) | Highest-Income (5th Quintile) | ||||

|---|---|---|---|---|---|---|

| 1997-98 | 0.3% | 1997-00 Annual Average:-3.5% | 4.3% | 1997-00 Annual Average:0.7% | 5.6% | 1997-00 Annual Average:0.3% |

| 1998-99 | -0.8% | -1.0% | -4.0% | |||

| 1999-00 | -9.7% | -1.0% | -0.4% | |||

| 2000-01 | 5.4% | 2000-07 Annual Average:1.2% | 1.3% | 2000-07 Annual Average:2.4% | 1.1% | 2000-07 Annual Average:2.5% |

| 2001-02 | 7.9% | 3.7% | 6.7% | |||

| 2002-03 | 4.2% | 6.1% | 4.3% | |||

| 2003-04 | 4.8% | 5.2% | 1.6% | |||

| 2004-05 | -13.0% | -3.5% | -0.3% | |||

| 2005-06 | -11.4% | -3.9% | -0.4% | |||

| 2006-07 | 14.0% | 8.6% | 4.7% | |||

| 2007-08 | 2.8% | 2007-12 Annual Average:3.5% | 3.0% | 2007-12 Annual Average:3.2% | 1.1% | 2007-12 Annual Average:2.6% |

| 2008-09 | 1.9% | 5.6% | 6.0% | |||

| 2009-10 | 0.04% | -3.1% | 2.3% | |||

| 2010-11 | 12.8% | 7.4% | 1.8% | |||

| 2011-12 | 0.5% | 3.3% | 2.2% | |||

| 2001-12 (Average) | 1.0% | 2.3% | 2.1% | |||

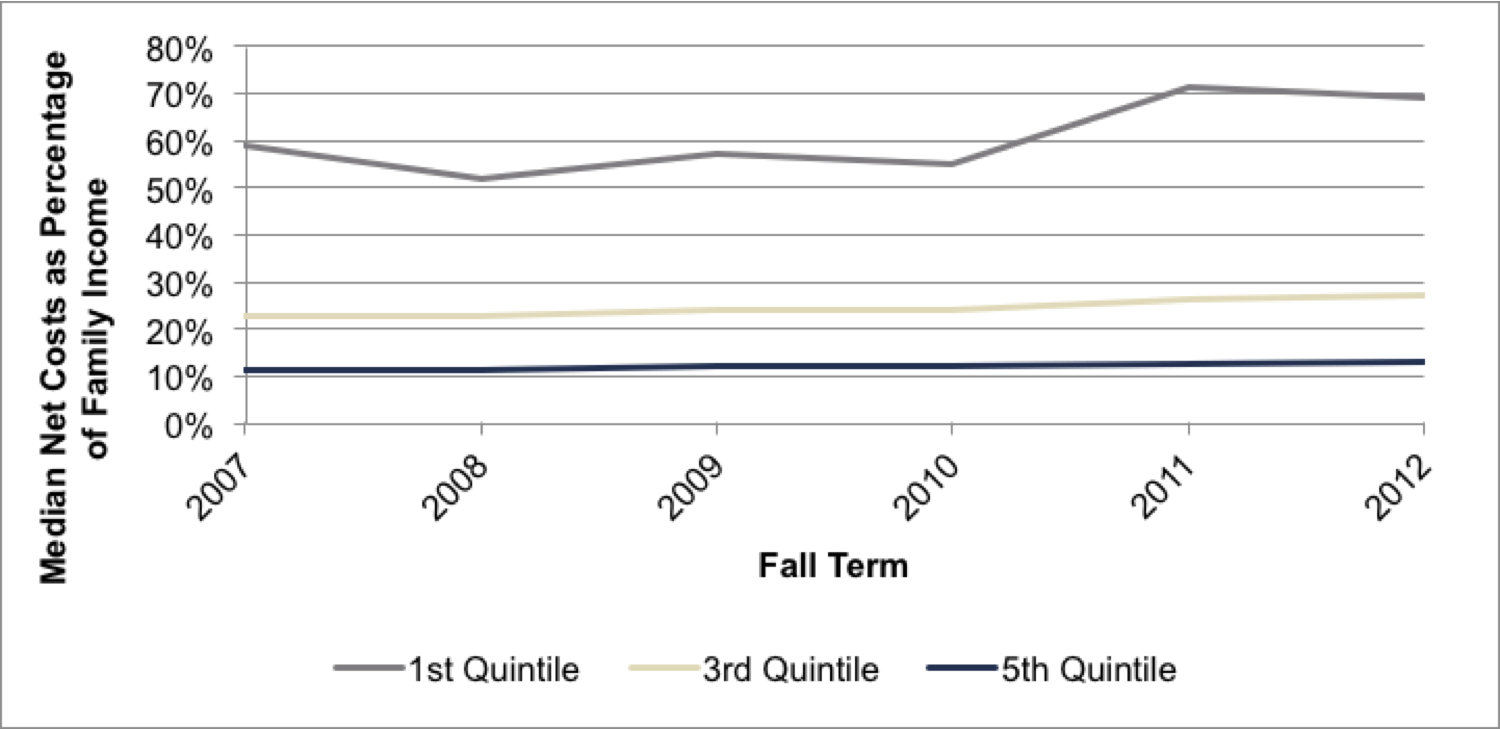

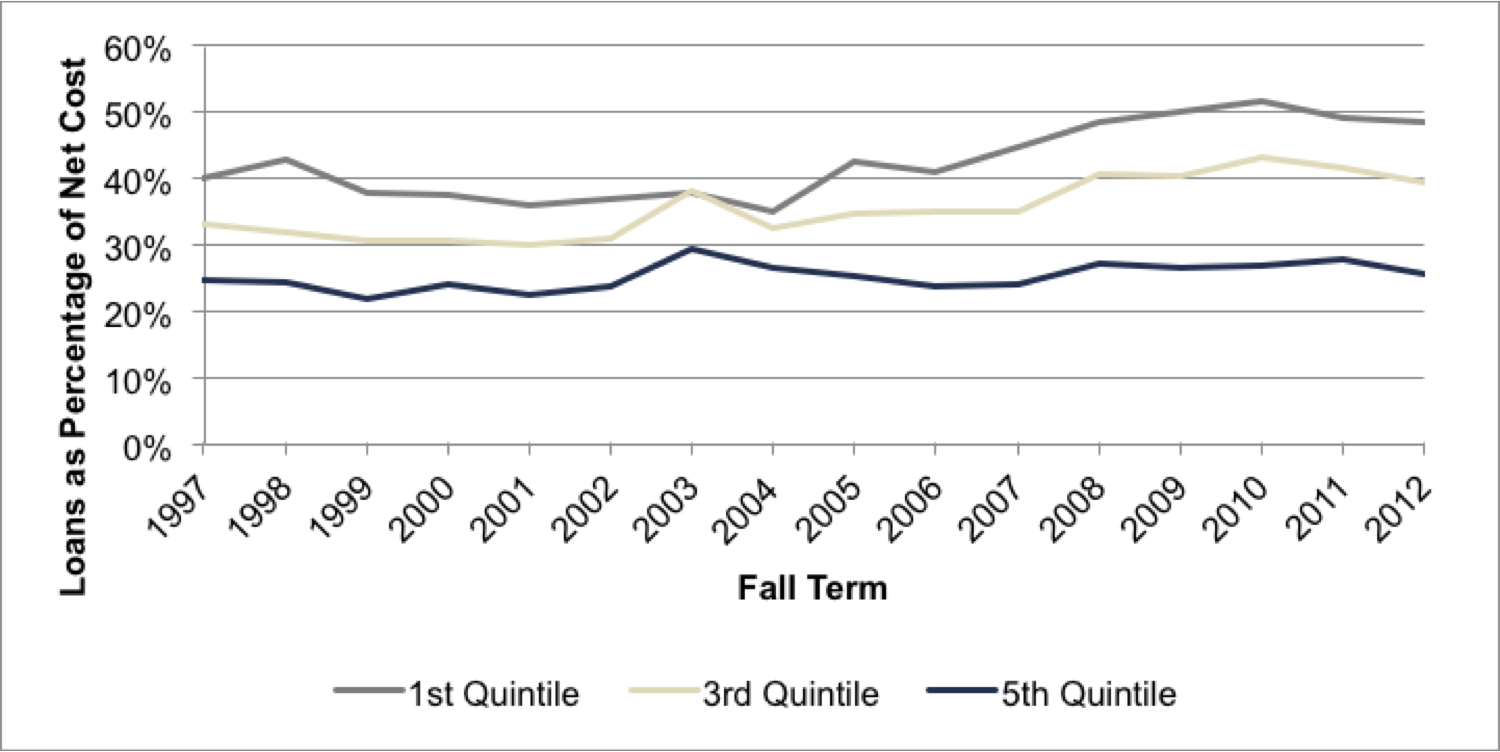

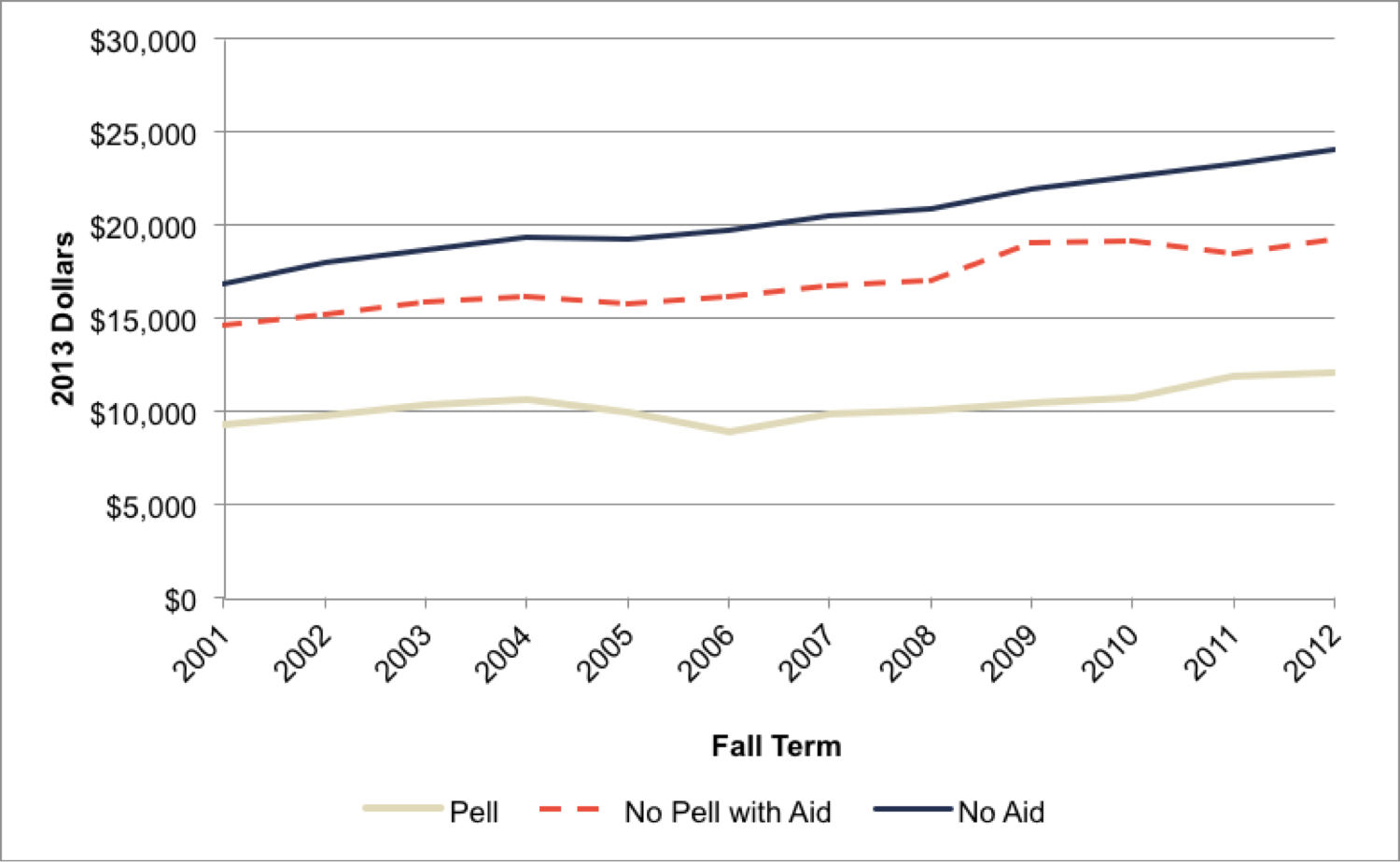

Since 2007, the growth in net costs has also outpaced growth in family incomes for students in all income quintiles, with the exception of those in the highest quintile (Figure 3.2).[47] By 2012, net costs for the median poor and near-poor student constituted 69% and 27% of their respective annual family incomes, while the comparable burden of net costs comprised only 13% of family income for the median highest-income student. These patterns may explain why student borrowing is so prevalent among students in lower income subgroups. Indeed, Figure 3.3 shows that poor students and near-poor students since 2007 have been taking out loans to finance on average 49% and 40%, respectively, of their annual net costs, (contrasted with pre-2007 rates of 39% and 33%). Given the increasing reliance on loans that have accompanied the increases in net costs since the Great Recession, there is ample reason to be worried about how these financial burdens will influence student outcomes over time.

Figure 3.2. Median Net Costs as Percentage of Family Income

Figure 3.3. Average Loans as Percentage of Net Costs

In summary, we find clear evidence that net costs at Virginia’s public four-year institutions have grown significantly for poor and near-poor students since 2007 (in comparison to both previous years and the rates experienced by their highest-income peers), with these increases accelerating in the most recent years. Furthermore, we find that these patterns persist even after defining student subgroups in different ways (see Section A.1 of the Appendix). These inflation-adjusted increases have, in turn, placed greater financial burdens on those poor and near-poor students and families already struggling to afford a public college education. In later sections, we will examine how these burdens may be influencing student progress towards a degree.

Differences in Trends across Institutions

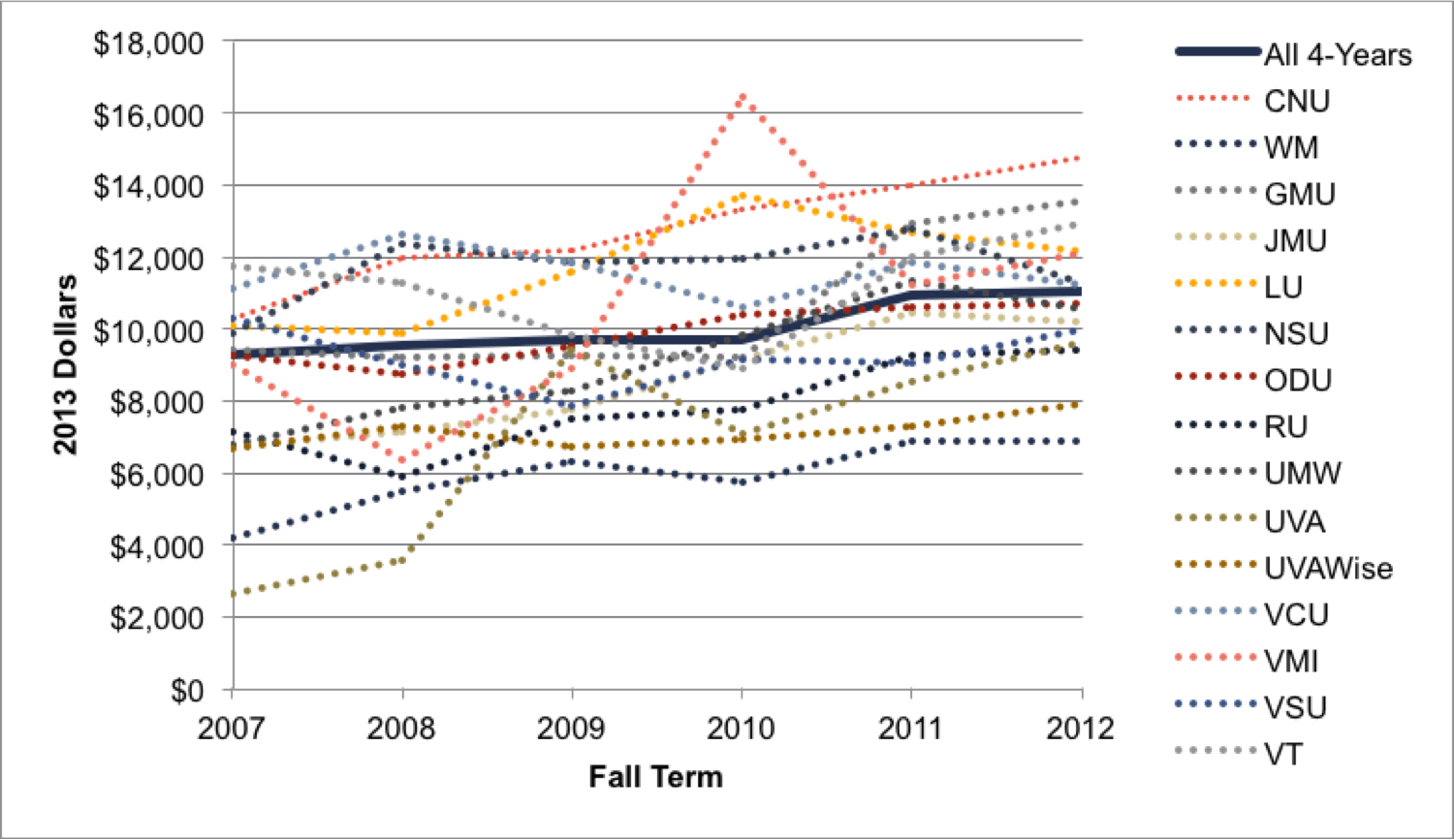

Next, we disaggregate the net cost trends at the institutional level. Our goal here was not to understand all of the nuances associated with changes at each institution, but rather to confirm that the average trends we observed were prevalent across the entire system and not driven by only a few institutions. Indeed, we found – albeit to varying degrees and with slightly different patterns – that significant increases in net costs for poor and near-poor students have occurred since 2007 at almost every institution.

Figures 3.4a and 3.4b illustrate the respective trends in net costs for poor and near-poor students at each institution since 2007, overlaid by the average trends that we showed earlier. Net costs have increased for poor and near-poor students at almost every institution during this time period, with only a few outliers. While the patterns for poor students seem slightly more scattered, Table 3.3 indicates that these patterns have also begun to converge in the most recent years.[48] The patterns for near-poor students appear to be more clustered, and Table 3.3 confirms yet again that these trends did not significantly diverge even as net costs continued to increase. Thus, we find evidence that the recent increases in net costs for poor and near-poor students occurred across the entire group of public four-year colleges and universities.

Figure 3.4a. Institution-Level Net Costs for Poor Students

Figure 3.4b. Institution-Level Net Costs for Near-Poor Students

Table 3.3. Standard Deviation between Institutions in Rates of Change for Net Costs

| Poor (1st Quintile) | Near-Poor(3rd Quintile) | |

|---|---|---|

| 1997-2007 (Average) | 0.20 | 0.09 |

| 2007-08 | 0.18 | 0.09 |

| 2008-09 | 0.15 | 0.05 |

| 2009-10 | 0.13 | 0.07 |

| 2010-11 | 0.17 | 0.13 |

| 2011-12 | 0.07 | 0.04 |

Changes in the Components of Net Costs

We now examine how changes in the components of net cost – namely, tuition and various sources of gift aid – have interacted to produce the overall increases in net costs documented thus far. Concentrating on poor and near-poor students since 2007, we carried out this analysis for the set of all four-year institutions, as well as for LDS and HDS institutions separately. Because LDS and HDS schools have attempted to cope with declining state support in somewhat different ways (see Section 2), we were interested in seeing to what extent there exist structural differences between the two groups with regard to whether and how they have shifted the financial burdens onto their students.

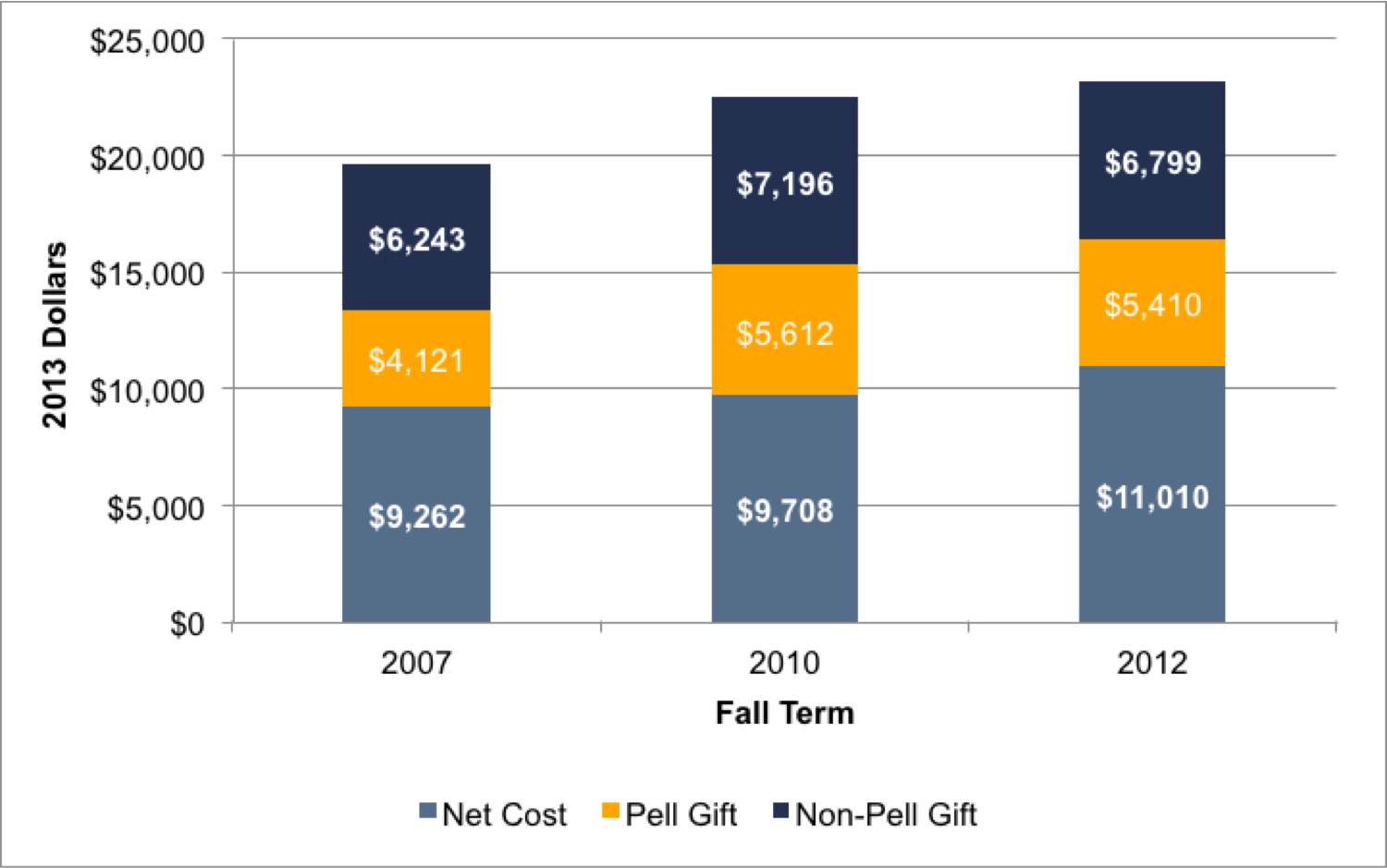

For poor students at all four-year institutions, average net costs grew by less than $400 between 2007 and 2010, a surprisingly modest number given the financial challenges these institutions faced. Figure 3.5a shows that the growth in average gift aid during this time period (spurred by a large increase in the average Pell Grant) was nearly enough to offset the growth in average student charges. From 2010 to 2012, the growth in student charges actually moderated somewhat, but the large reductions in both sources of gift aid (state/institutional aid and Pell Grants) that occurred simultaneously led to the dramatic increase in net costs that we observed in Figure 3.1 and Table 3.2.[49]

Figure 3.5b tells a similar story for near-poor students across all four-year institutions, with average gift aid rising from 2007 to 2010 but then falling slightly from 2010 to 2012, even as student budgets increased throughout. Note that Pell Grants make up a smaller fraction of total gift aid for near-poor students, who therefore did not benefit from as large an increase in gift aid as poor students did from 2007 to 2010 (when Pell Grants considerably increased in value). Consequently, near-poor students faced a substantial increase in net costs from 2007 to 2010 and an even larger increase from 2010 to 2012 when state and institutional gift aid declined.

Figure 3.5a. Components of Overall Net Costs for Poor Students

Figure 3.5b. Components of Overall Net Costs for Near-Poor Students

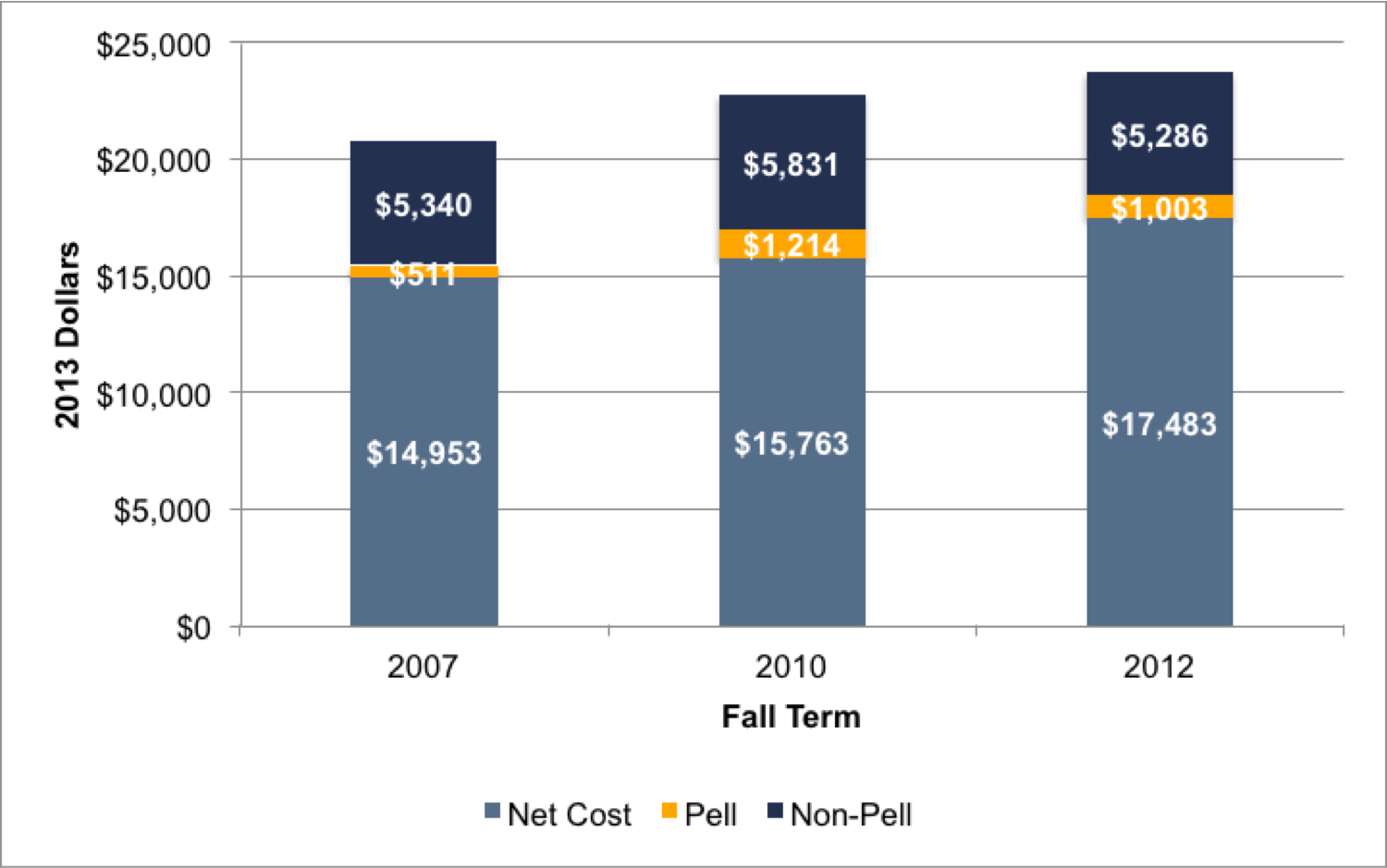

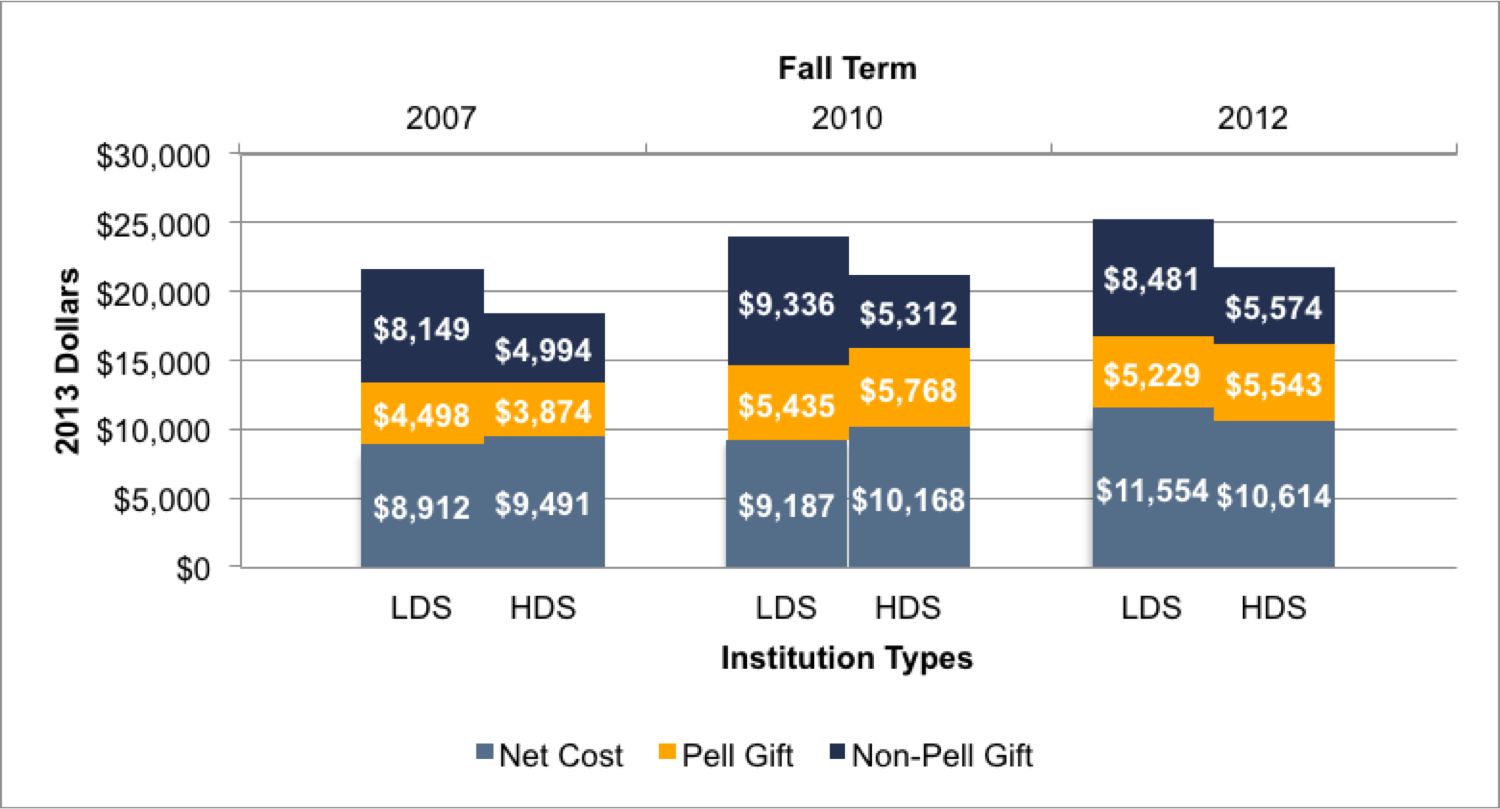

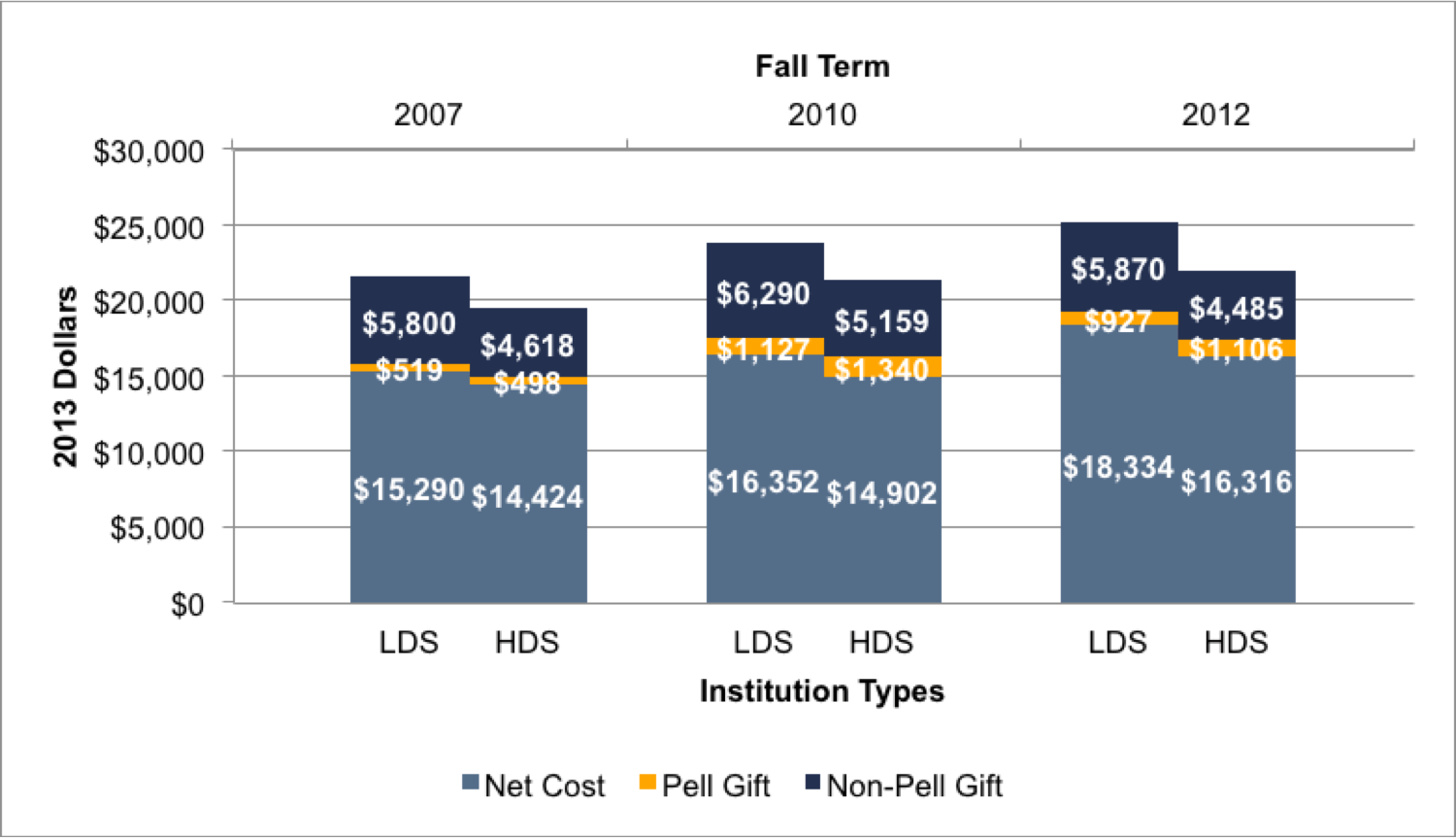

These general patterns seem most intense among LDS institutions, which instituted both larger increases in student charges and saw greater reductions in gift aid between 2010 and 2012 than their HDS peers. Indeed, 2012 marked the first year in which average net costs for poor students in our sample were lower at HDS institutions than at their LDS counterparts, as the traditionally high levels of gift aid at LDS institutions had until recently kept pace with their consistently higher student budgets (Figure 3.5c). Similarly, while net costs have always been greater at the LDS institutions for near-poor students, the difference in net costs between LDS and HDS institutions for the near poor has continued to increase in the most recent years (Figure 3.5d).

Figure 3.5c. Components of LDS and HDS Net Costs for Poor Students

Figure 3.5d. Components of LDS and HDS Net Costs for Near-Poor Students

In summary, student charges have increased significantly faster than inflation at all institutions since 2007, while the growth in financial aid for poor and near-poor students has been slower and less consistent. In particular, the decline in gift aid for these students from 2010 to 2012 resulted in significant increases in net costs that outpaced increases observed in previous years. Because gift aid generally constitutes less than half the amount of student budgets for both poor and near-poor students, financial aid would have had to grow at more than twice the rate of student charges in order to completely offset tuition increases. Anything less – let alone the flattening or declining rates of change for gift aid that occurred in the most recent years – results in an increase in net costs for these students, thus threatening the ability of poor and near-poor students to finance their education. Indeed, we calculated that total financial aid across all four-year institutions would have had to increase by $11.4 million for poor students and $20 million for near-poor students to merely hold the students in our sample harmless just from the increases in student charges between 2007 and 2012.[50]

The growth in net costs since the onset of the Great Recession, and particularly for the poorest students in recent years, raises questions about how these costs are influencing student decisions to pursue and earn a degree. We hypothesize that the increasing burden that poor and near-poor students and their families must bear in order to finance a post-secondary education may very well impact whether or not these students pursue a four-year degree and how steadily they move towards achieving that degree. In the next section, we look at trends in student enrollment, first-year retention, and four-year graduation rates to see if there are any patterns that may be readily linked to the growth in net costs. In the subsequent section, we employ multivariate regressions to examine more rigorously how net costs are related to student outcomes.

Section 4: Trends in Student Enrollment, Retention, and Graduation

The growth in net costs since 2007, especially for the poorest students, raises important questions regarding how these costs are influencing student decisions to enroll at a public four-year institution, remain enrolled, and complete a degree in a timely manner. In this section, we look at patterns in student enrollment, first-year retention, and four-year graduation between 1997 and 2012 to see if there have been any changes that may be tied to trends in net costs.[51]

Enrollment

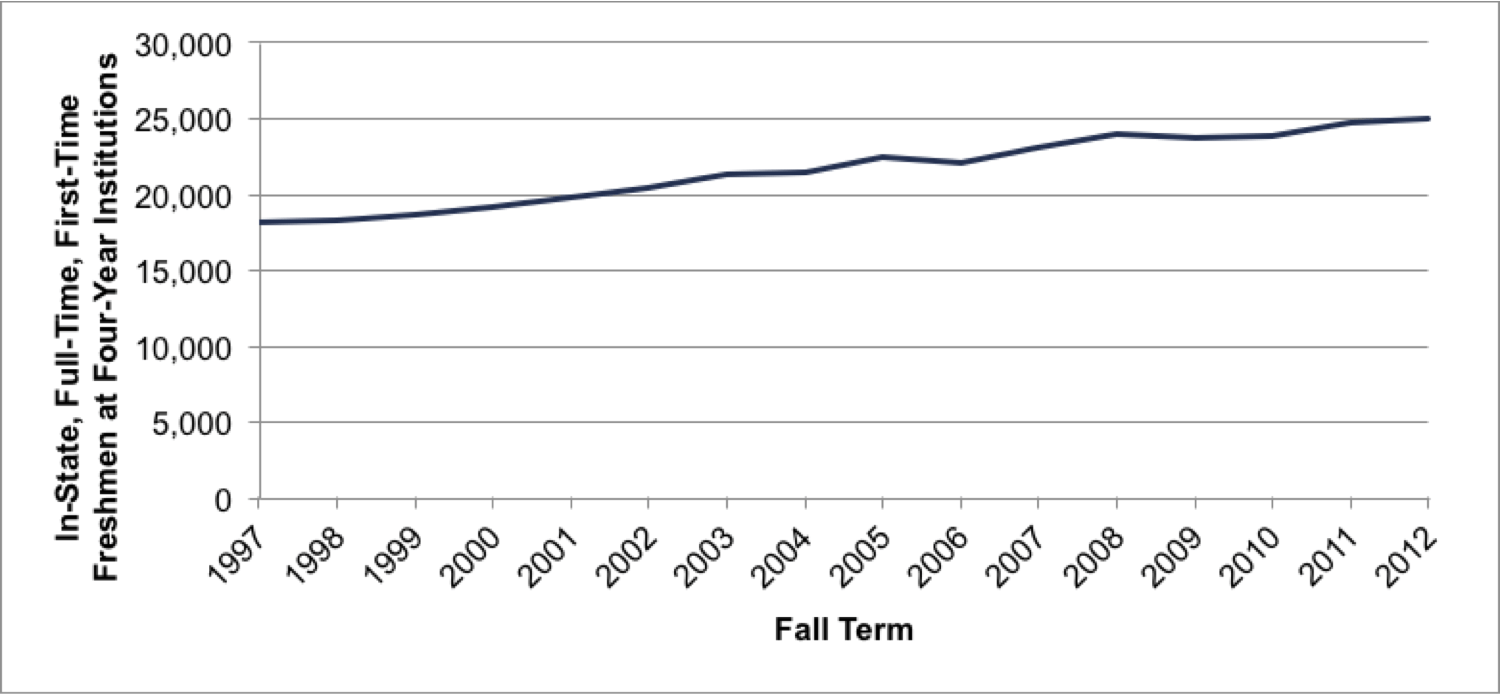

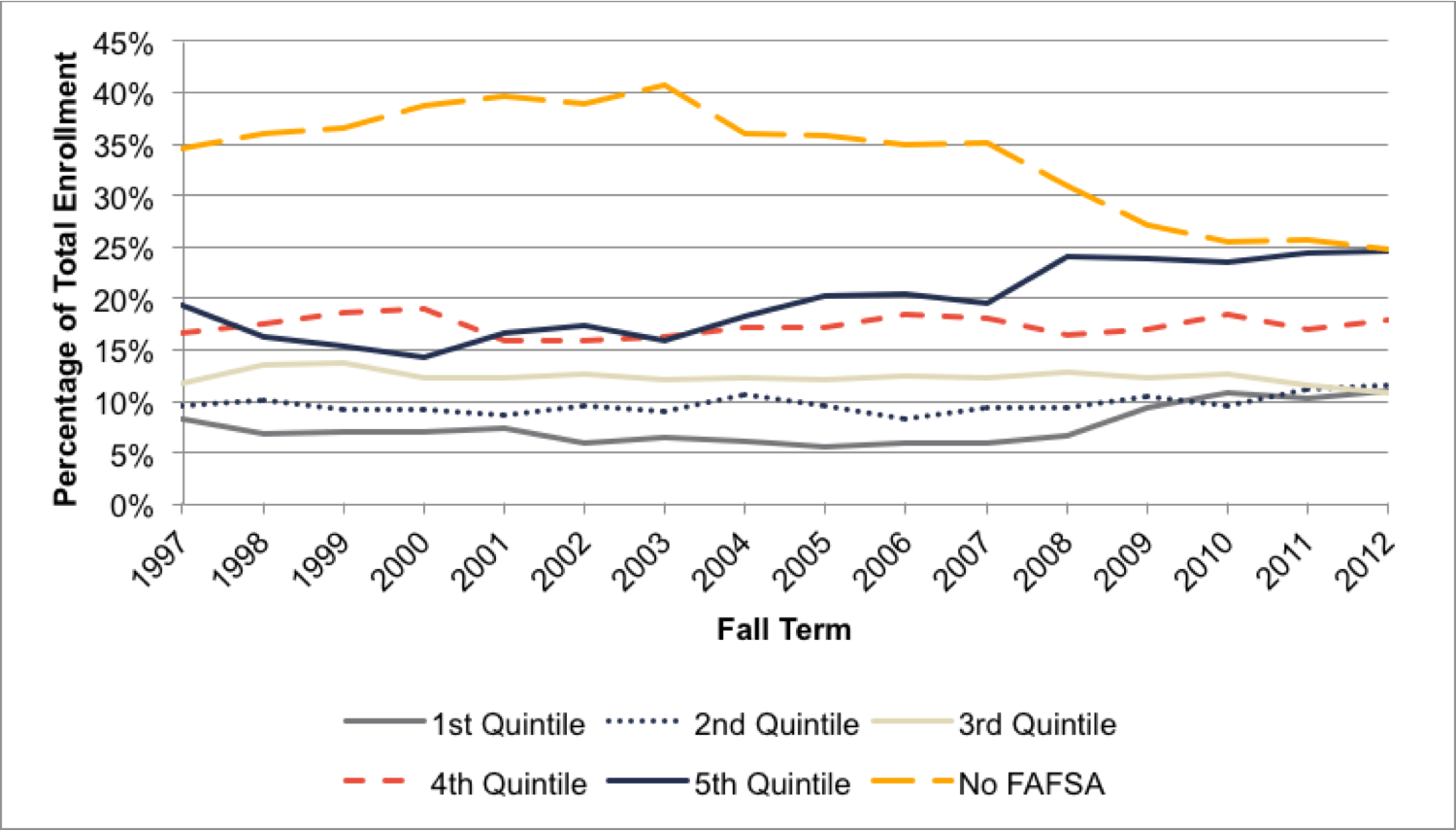

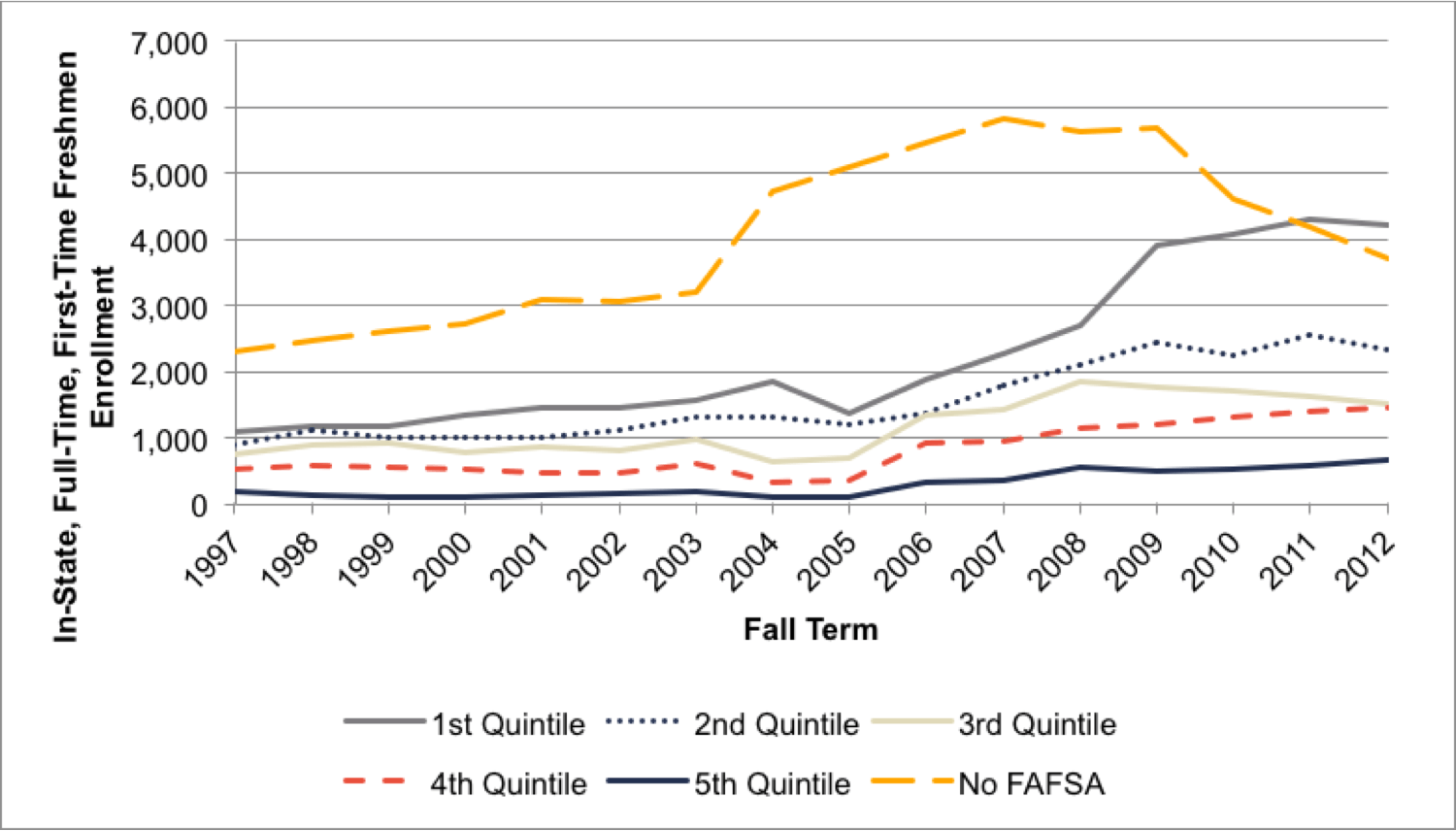

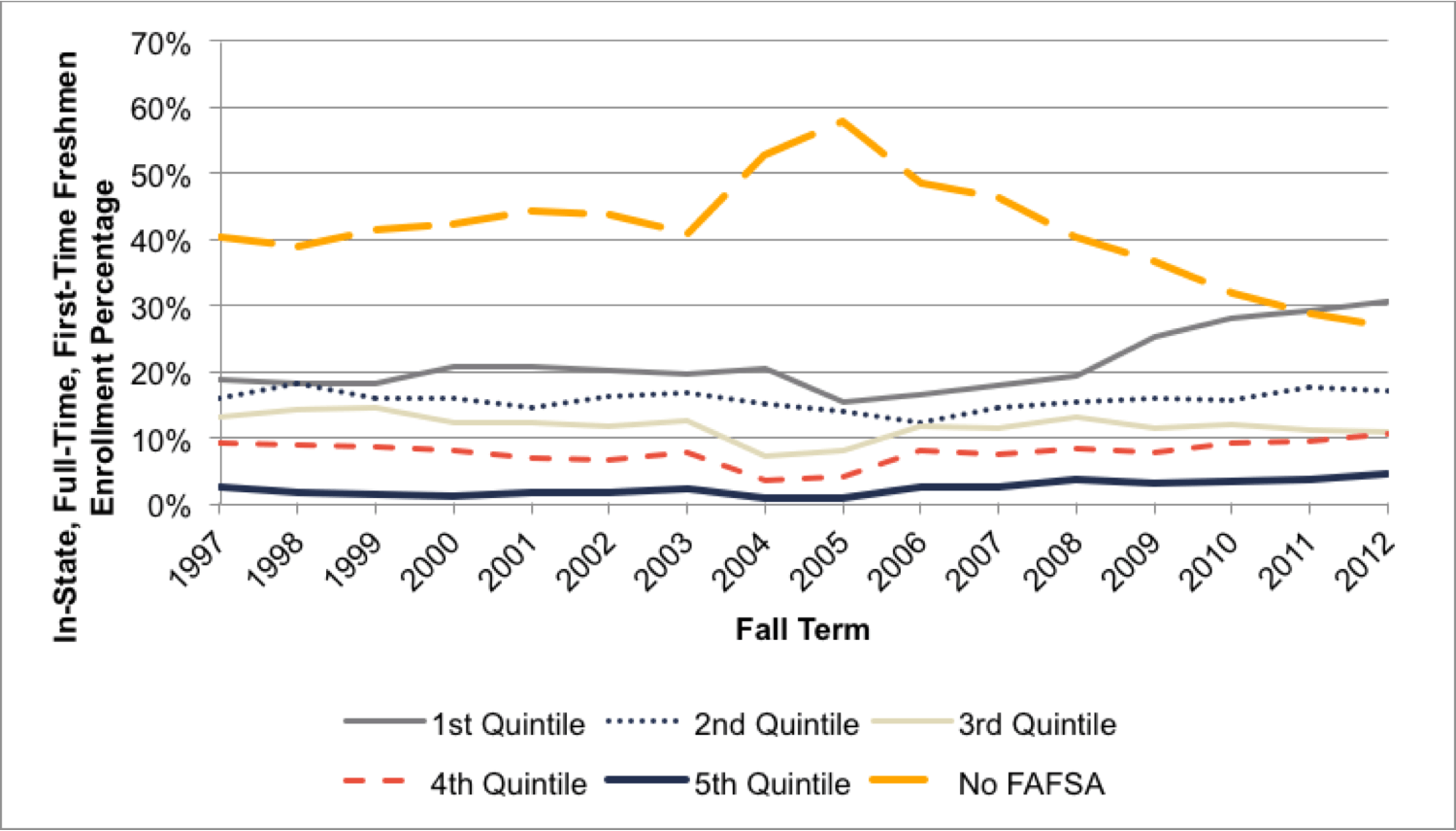

Since 1997, the total enrollment of students in our sample (in-state, first-time freshmen enrolling on a full-time basis at public four-year institutions) has increased at an average rate of 2.5% per year, although this growth rate has slowed slightly since 2007 to an average of 1.5% per year (Figure 4.1).[52] Figures 4.2 and 4.3 break down the overall enrollment trend by income quintile, with the former showing overall enrollment numbers and the latter indicating enrollment percentages by quintile.[53] Since 2007, there has been a significant increase in the enrollment of students who filled out FAFSA forms and a corresponding decrease in the number of students who did not fill out a FAFSA. While it is hard to identify cause-and-effect relationships, it appears that the sharp decrease in “No FAFSA” students from 2007 to 2008 occurred simultaneously with a substantial increase in the number of students from the 5th income quintile who decided to apply for financial aid. Since 2010, however, enrollments across all income quintiles have largely remained flat. As a result, while there are clearly many more factors at work during these years in addition to rising net costs (for example, the improving job market), enrollment among students in the lower-income quintiles has stopped growing and remains well below the enrollment numbers of their higher-income peers.

Figure 4.1. Total Enrollment

Figure 4.2. Enrollment Numbers by Income Quintiles

Figure 4.3. Enrollment Percentages by Income Quintiles

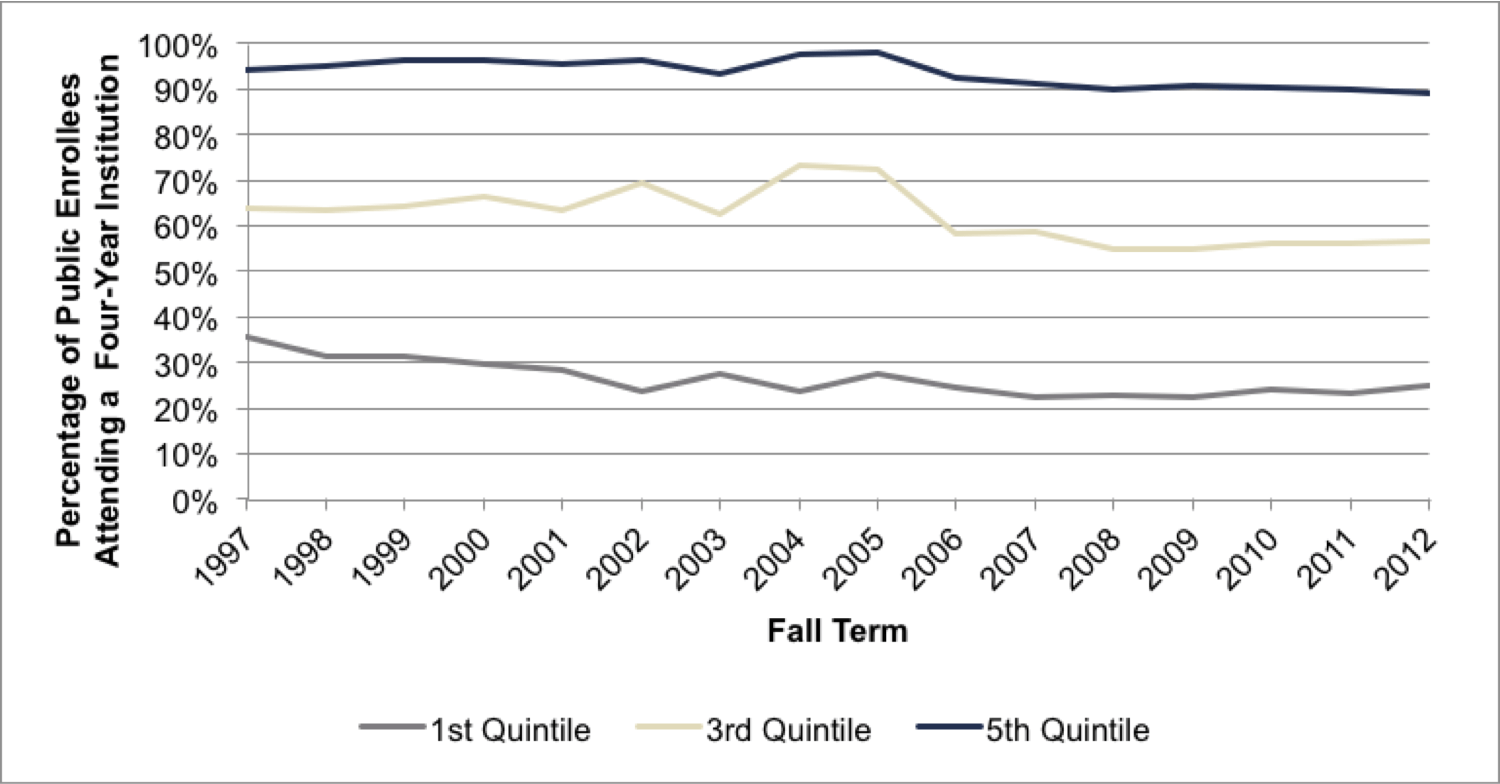

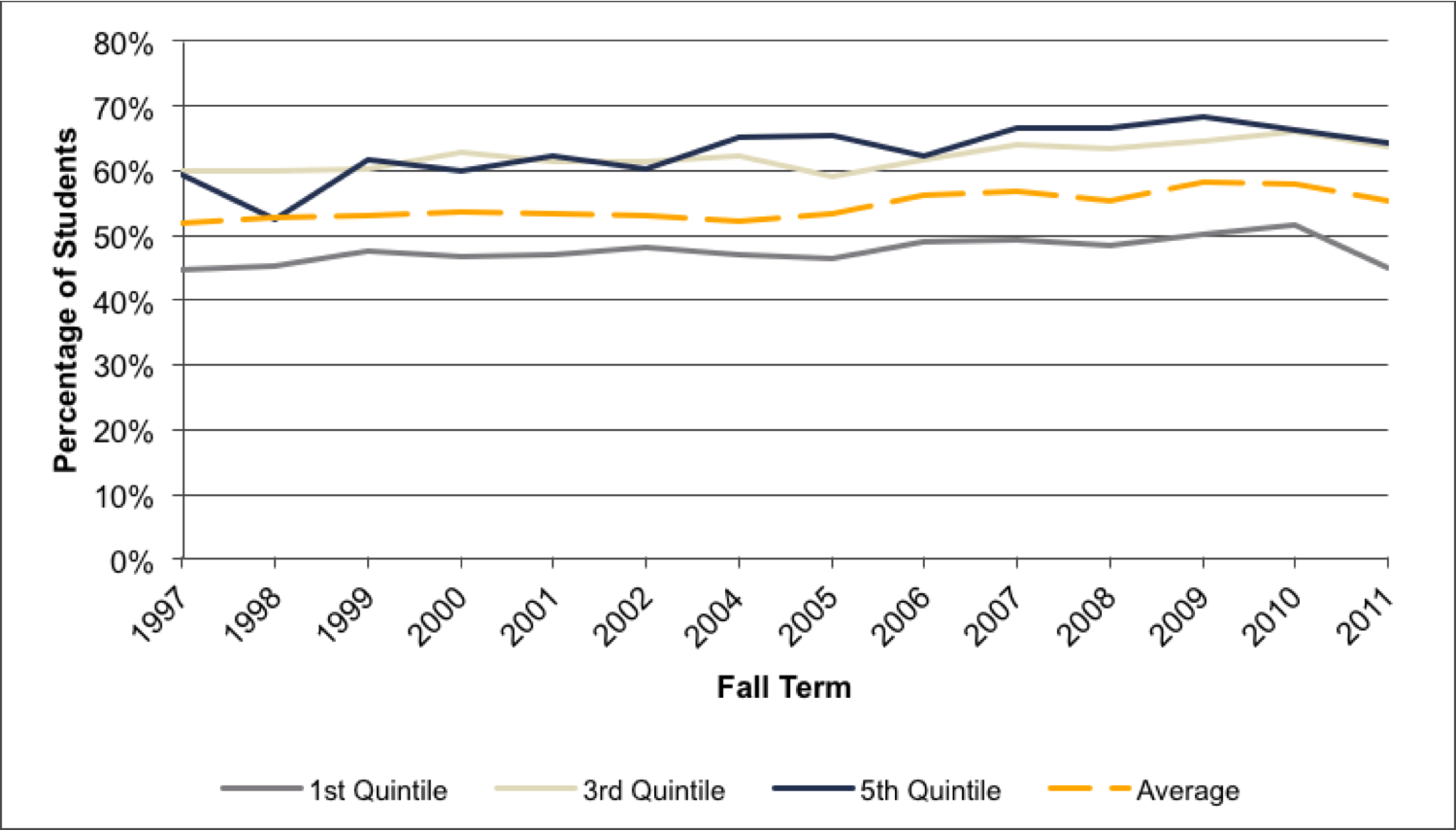

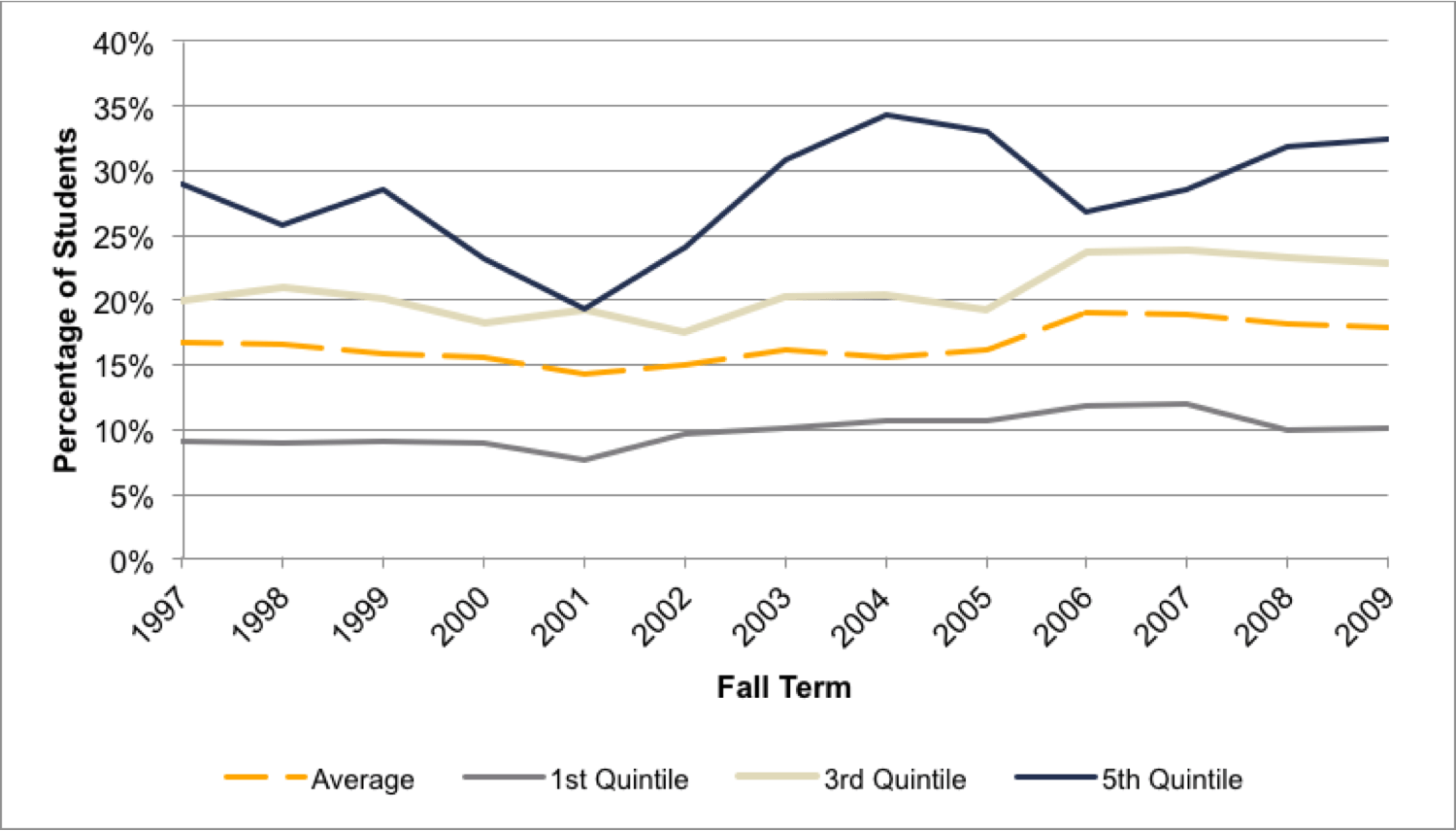

Figure 4.4 frames these enrollment trends in a different – and more troubling – context, showing enrollments among poor, near-poor, and highest-income students at four-year public institutions as percentages of total enrollment among each income subgroup in any public Virginia institution of higher education (public four-year and two-year).[54] Since 2007, these patterns have remained largely unchanged for all of these subgroups, with approximately 90% of all highest-income and 56% of near-poor public college enrollees in Virginia starting at a four-year institution. This level drops significantly for the poor, for whom only 23% of all public college enrollees since 2007 initially enrolled at a four-year school, with this percentage having steadily declined from a high of 35% in 1997.[55] These trends suggest that, since 2007, there has been no progress in shrinking the very large socioeconomic gap among entering students in terms of attendance at four-year institutions. Students in the lowest-income quintile – in contrast with their higher-income peers – are still overwhelmingly likely to enroll in a public two-year institution and not a four-year institution.

Figure 4.4. Enrollment at Four-Year Institutions as Percentage of Total Statewide Enrollment

Relatively few students who start at a two-year institution earn an associate’s degree, and even fewer transfer to a four-year institution and ultimately earn a four-year degree.

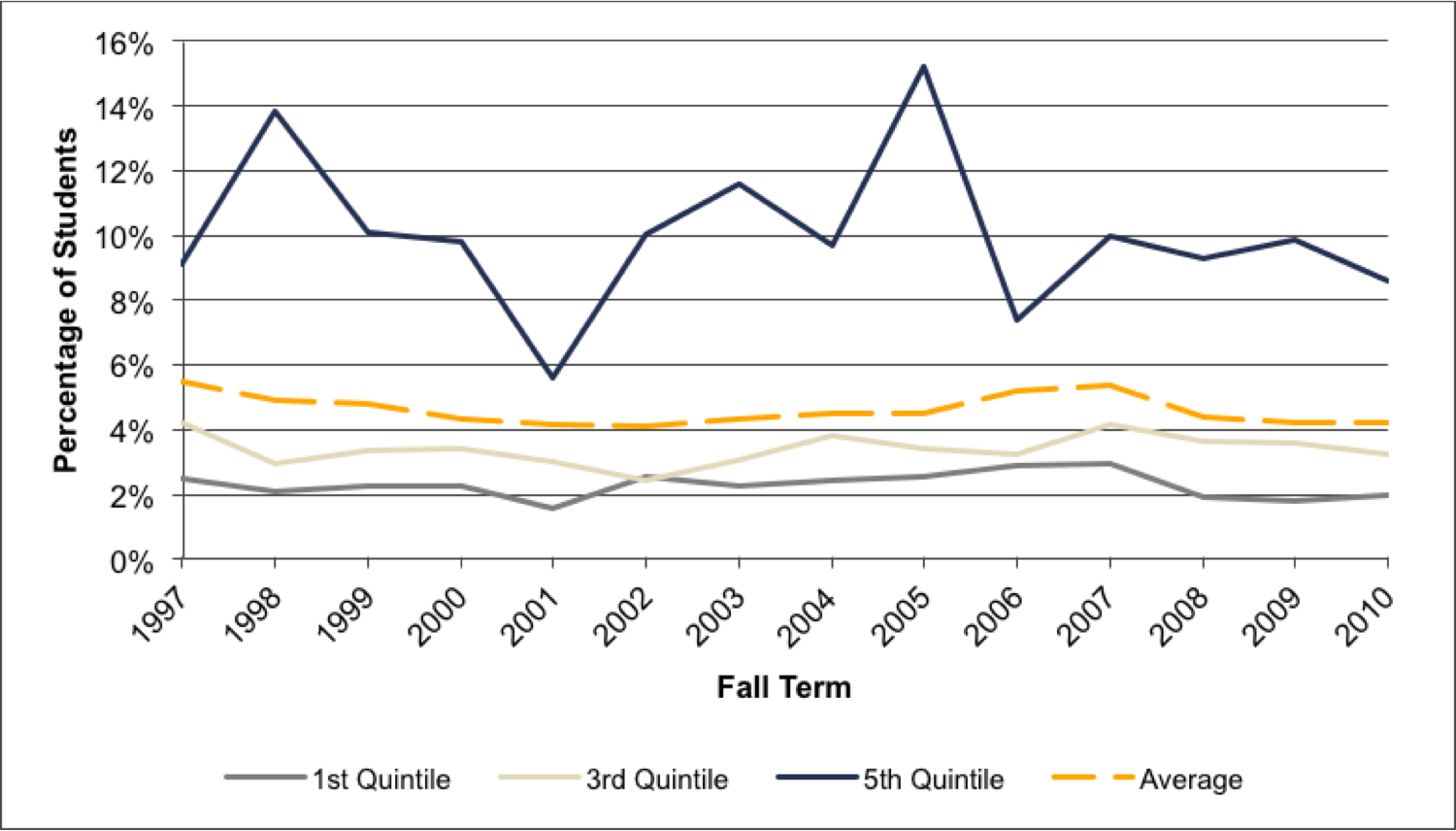

This is particularly troubling since success rates are much lower for students who start at a two-year school compared to those who start at a four-year school – even for those who enroll on a full-time basis. As Table 4.1 indicates, relatively few students who start at a two-year institution earn an associate’s degree, and even fewer transfer to a four-year institution and ultimately earn a four-year degree. If differences in net costs push large numbers of students to attend two-year institutions instead of four-year institutions, there is a significant reason to be concerned about these students’ prospects for earning a bachelor’s degree. If we are to make progress in increasing the overall number of college graduates and narrow the existing gaps between socioeconomic groups, it is important to both address the costs of earning a degree and raise the success rates of students attending community colleges.

Table 4.1. Success Measures by Original Institution Type and Full-Time Status

| Retained for a Second Year | Earned a Bachelor’s Degree in 4 Years | Earned a Bachelor’s Degree in 6 Years | Earned an Associate’s Degree in 2 Years | Earned an Associate’s Degree in 3 Years | Transferred to Four-Year Inst. within 2 Years | Earned an Associate’s or Transf. to a Four-Year Inst. within 3 Years | |

|---|---|---|---|---|---|---|---|

| Four-Year Full-Time | 84% | 42% | 66% | ||||

| Four-Year Part-Time | 67% | 27% | 39% | ||||

| Two-Year Full-Time | 54% | 2% | 5% | 5% | 12% | 5% | 18% |

| Two-Year Part-Time | 37% | 3% | 4% | 3% | 7% | 3% | 10% |

Retention Rates

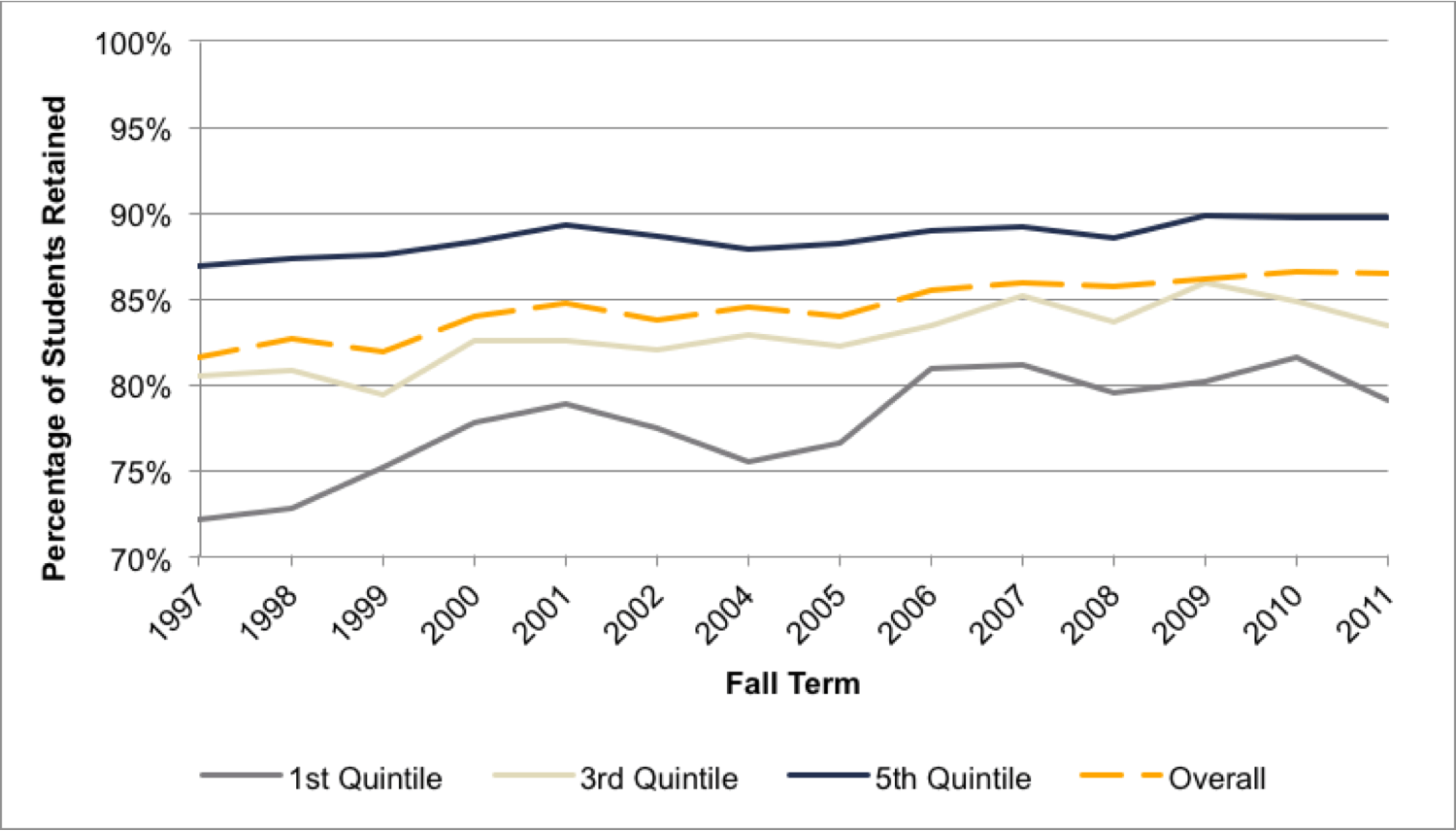

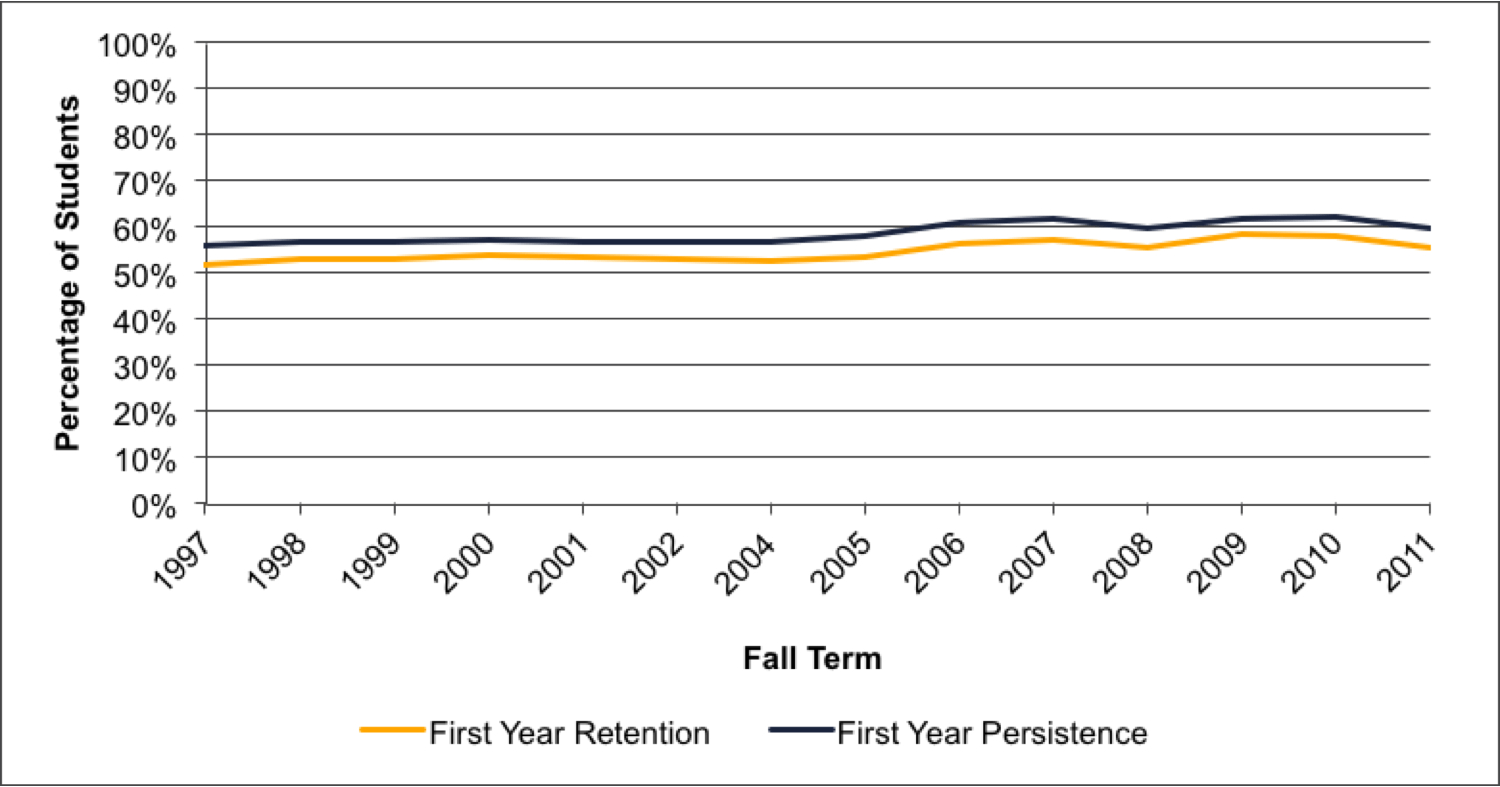

We find similar patterns in student progress towards a degree. Overall first-year retention rates among first-time, full-time students at public four-year institutions have increased slightly since 1997 but have hovered around an average of 85% (Figure 4.5). The breakdown by income quintiles shows that the highest income students are on average 11 percentage points more likely to be retained than the lowest income students, and 6 percentage points more likely than students in the 3rd income quintile. Thus, even among the few low-income students who begin as full-time students at 4-year institutions, the chances of persisting are less than those of their higher-income peers.

We see similar trends for first-year persistence (which includes all students who were retained or transferred), though the rates are slightly higher (91%) because transfer students are counted as persisting. Of the 15% of students who are not retained after the first year, approximately 40% transfer, 29% drop out, and 31% take time off.[56] These shares have remained relatively stable over this period as well.

Figure 4.5. First-Year Retention Rates

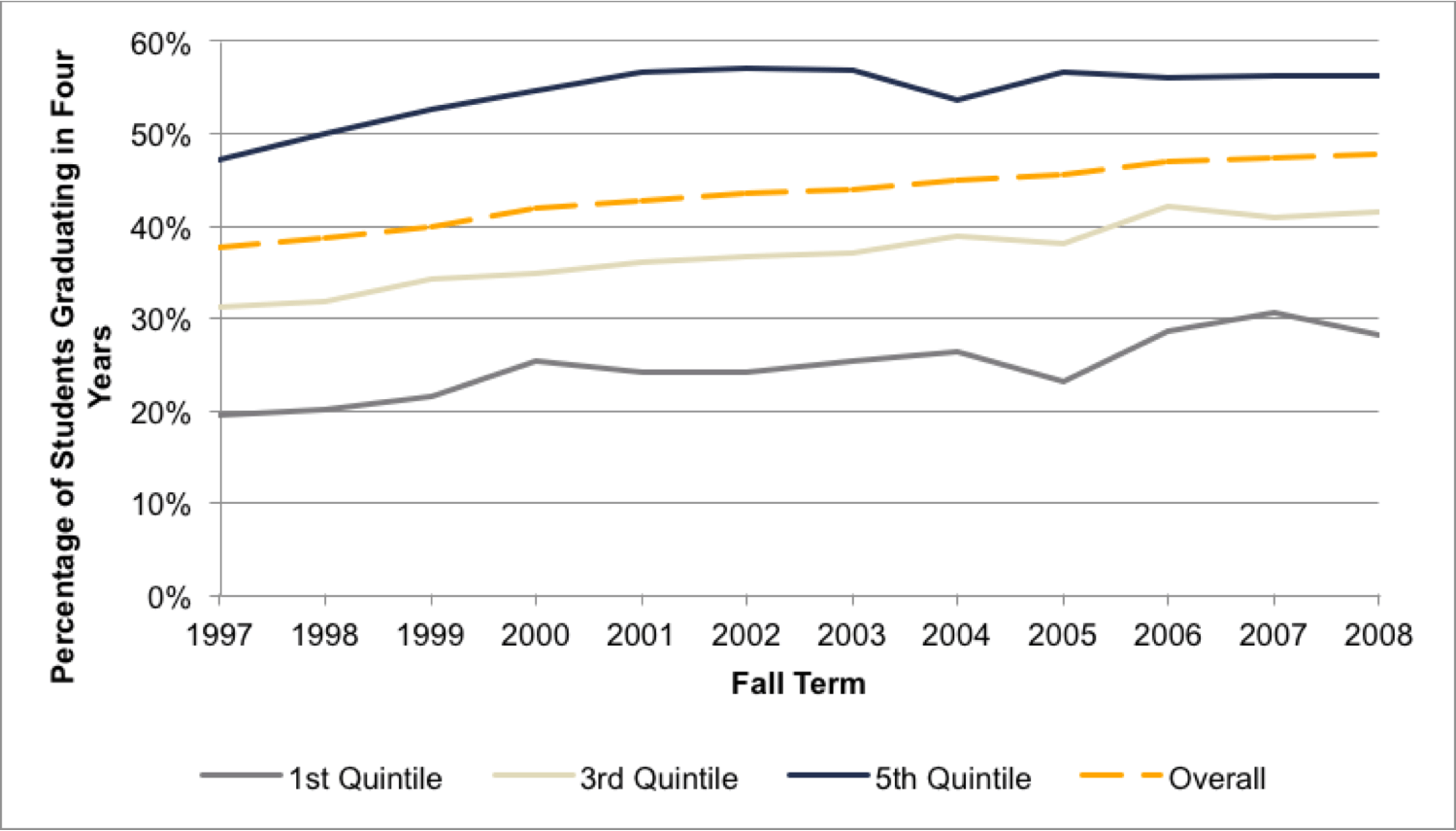

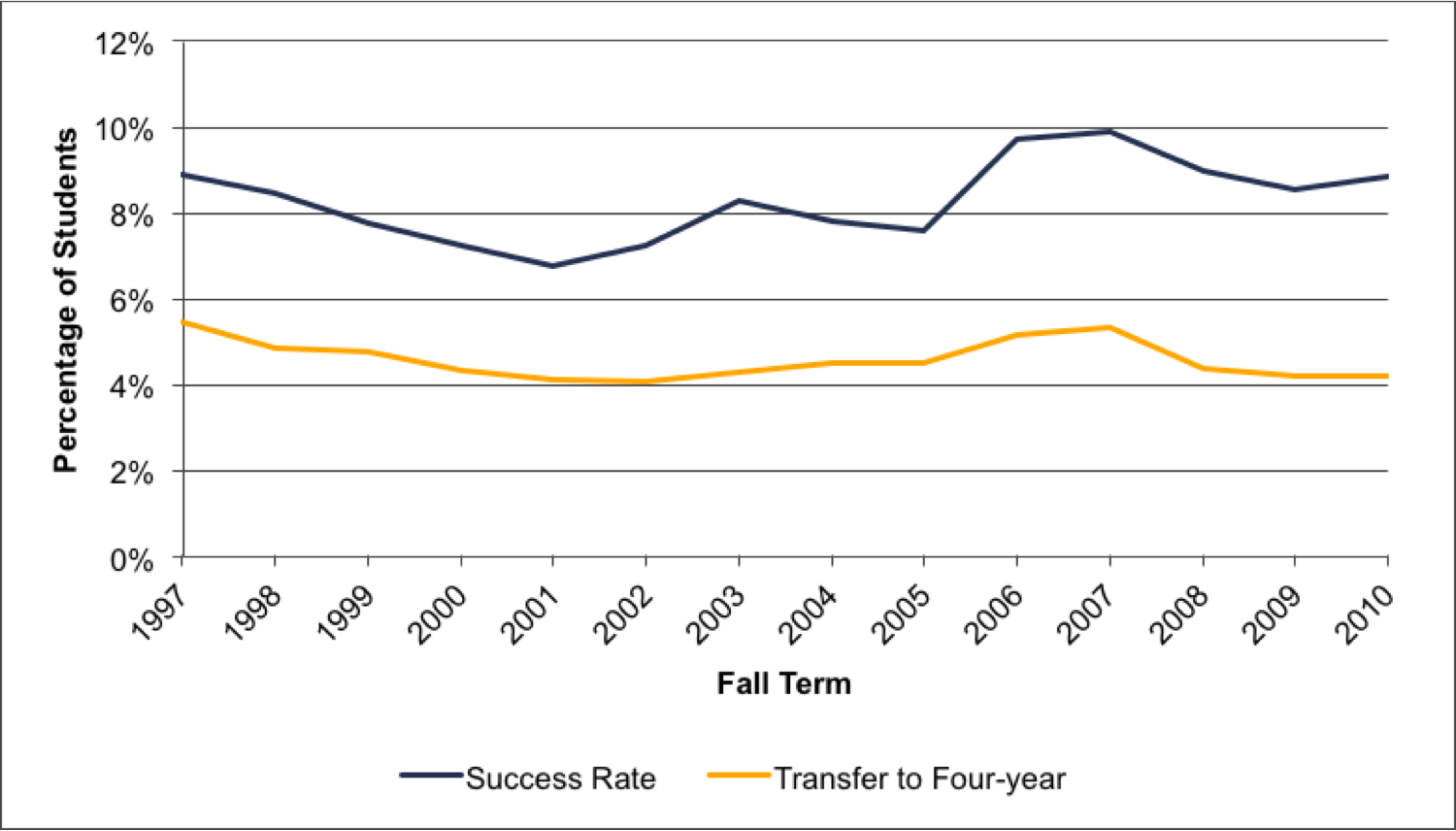

Four-Year Graduation Rates

The overall four-year graduation rate has been increasing since 2001, from 37% for the cohort that entered in 1997 to 48% for the cohort that entered in 2008. While these increases have occurred for both the lowest and highest income groups, it is important to note that the gap in graduation rates between the 1st and 5th income quintiles has not closed over time and has instead held roughly stable at about 30 percentage points per year (Figure 4.6). Indeed, this gap was 28 percentage points for both the cohort entering in 1997 and the cohort entering in 2008. This strongly suggests that we have fallen well short of achieving the stated goal of “equal opportunity for all” throughout this period. While we do not have graduation rate data for later cohorts, there is little reason to believe that progress has been made since 2008. In fact, the data on retention rates and other success measures suggest that, if anything, we are headed in the opposite direction.

Figure 4.6. Four-Year Graduation Rates

While we do not see significantly worsening trends in student outcomes and enrollment in light of rising net costs since 2007, it is clear that the current levels are not improving at the rate they would need to in order to achieve national and state goals for higher education. This is especially true for low-income students, who are significantly less likely to enroll at four-year institutions in the first place, and also less likely to re-enroll for a second year. We fear that the increases in net costs we have seen – and expect to continue seeing – will further reduce these students’ likelihood of success. We test this hypothesis in our next section, where we employ regression methods to examine how increases in net costs – holding other factors constant – are related to changes in student retention, persistence, credit completion, and graduation.

Section 5: Descriptive Analysis of the Impact of Rising Net Costs on Student Success

Against the backdrop of continuing growth in net costs, this section presents the results of multivariate regression analyses designed to determine the extent to which the increases in net costs have affected student patterns in enrollment and degree completion.[57] These regression techniques hold constant a variety of student characteristics, in addition to controlling for institution- and year-fixed effects. Using first ordinary least squares (OLS) regression techniques, we find that net costs are negatively related to student re-enrollment at the same or another institution after the first year, the number of credits completed, progress towards a four-year degree, and graduation in four years. These effects are statistically significant and largest for the poorest students, who have also seen the fastest growth in net costs since 2007 and have the lowest retention and graduation rates to begin with.

We will report in the next section on a difference-in-differences quasi-experiment which exploits an exogenous change in expected family contribution (EFC) rules for certain low-income students to estimate the causal impact of a reduction in net costs on the success rates of those students. In that analysis, we find that a decrease in net costs has an even larger inverse effect on first-year retention than the effects we calculate via the OLS methodology. Taken together, these two sets of findings strongly suggest that the cumulative effect of continuing growth in net costs, holding other factors constant, will result in a substantial decline in student success rates and a further widening of the gap between success rates for students from different socioeconomic groups.

Methodology

For the OLS analysis, we examined a subset of the sample of first-time, full-time students at public four-year institutions that we analyzed in the previous sections. In particular, we limited our sample to those students who enrolled for an entire year and who entered in the fall term in order to ensure that we have accurate financial data for all students in our analysis. We also limited our sample to students who enrolled during and after 2004, since these are the only years in which data for SAT scores (which are needed to control for different levels of student preparedness) were collected. Finally, we dropped from our sample those students who did not file a FAFSA or who were missing EFC information.

In this section, we subdivided students based on their levels of EFC instead of income quintiles, given some complications with the income data and because EFC is the official metric used to determine a student’s gift aid. When not addressed, the potential errors in the income data (which include a number of students having low incomes and high EFCs or very different incomes between years) could bias the standard errors in our regressions and thus compromise some of our results. The greater reliability of the EFC data lends more credibility to the analysis of net costs and student outcomes when we break down the results by groups. However, it is important to note that these complications in the income data only appear to affect the student-level analyses done in this section and should not significantly bias the trends averaged across students reported in the previous sections. Indeed, the mean trends in net costs, enrollment, and outcomes for the EFC groups and income quintiles follow virtually identical patterns.[58]

Students are classified into four EFC quartiles based on the distribution within each year of first-year EFC levels for all students who entered a Virginia institution. The 1st EFC quartile is entirely composed of students with zero EFC and looks similar to the poor or low-income students referred to in previous sections. We characterize the 2nd EFC group as near-poor, and the 3rd and 4th quartiles as higher-income. Table 5.1 describes these groups in the context of their income distributions, with additional explanations of this classification method available in Section A.1 of the Appendix.

Table 5.1. Description of Income Levels by EFC Quartile

| Percentile within the EFC Quartile | EFC Q1 | EFC Q2 | EFC Q3 | EFC Q4 |

|---|---|---|---|---|

| 1% | $0 | $0 | $0 | $0 |

| 25% | $3,948 | $26,374 | $50,262 | $102,635 |

| 50% | $14,090 | $38,474 | $69,013 | $132,790 |

| 75% | $24,507 | $48,920 | $86,116 | $175,136 |

| 99% | $69,099 | $83,851 | $147,523 | $480,789 |

We employed a few different regression models in order to better understand the relationship between net costs and student success. We started with OLS regressions for our key outcome variables (first-year retention, first-year persistence, credits earned, progress towards a degree, and four-year graduation). In order to see how net costs influence these different measures of student success (holding all other factors constant), we included controls for student characteristics – including income at entry, EFC at entry, age, race, gender, SAT score, unemployment rate in the home zip code, campus housing status, and dependent status – as well as institutional- and year-fixed effects.[59] We then estimated regressions using both linear and non-linear specifications on net cost to see if students respond in different ways depending on their level of net cost, and we conducted a few robustness checks with different samples of the data. Next, we turned to a hazard model using a multinomial logistic regression, which enables us to compare all possible outcomes at the end of year one, as well as how net costs are associated with each path that a student can take (re-enrolling at the same institution, enrolling at another institution, and not persisting).[60]

Results

Table 5.2 presents the OLS regression results for first-year retention and first-year persistence, both of which are binary variables indicating whether or not a student was retained (at any institution) or persisted (at the same institution). The coefficients displayed denote the effect of an additional thousand dollars in net costs on student retention and persistence and represent changes in percentage points. The bottom line is that increases in net costs for each EFC quartile have a statistically significant, negative impact on student success.

Net costs have the largest impact on the poorest students. A $1,000 increase in net costs is associated with a 0.63 percentage point reduction in the likelihood of re-enrolling at any institution in the second year for students in the 1st EFC quartile (representing a reduction in the probability of being retained from 78.38% to 77.75%). While this effect appears small, it is statistically significant at the 99% confidence level – meaning that we can be 99% confident that the impact of increasing net cost is negative – and the cumulative effect of continuously rising costs can become large over time. Moreover, this result comes at a time when the goal is to reduce – not to increase – the gaps across subgroups.

We also look at first-year persistence rate (re-enrolling at the same institution) to ensure that the previous effect is not entirely driven by transfer students. For students in the 1st EFC quartile, a $1,000 increase in net costs reduces the probability of persisting into the second year by 0.54 percentage points. The effects decrease in magnitude for higher quartiles, but the coefficients on net costs are still negative and statistically significant at the 99% level for all four EFC quartiles. This suggests that, if net costs continue to increase at the rates we observed in Section 3, student retention and persistence rates will suffer – especially among the most disadvantaged students.

Table 5.2. Impact of a $1,000 Increase in Net Costs on First-Year Retention and Persistence

| First-Year Retention | First-Year Persistence | |

|---|---|---|

| $1,000 in Net Cost | ||

| EFC Q1 | -0.00631*** | -0.00537*** |

| (0.00088) | (0.00075) | |

| EFC Q2 | -0.00472*** | -0.00357*** |

| (0.00085) | (0.00069) | |

| EFC Q3 | -0.00446*** | -0.00280*** |

| (0.00061) | (0.00045) | |

| EFC Q4 | -0.00249*** | -0.00142*** |

| (0.00038) | (0.00024) | |

| Clustered standard errors are in parentheses. *** p<0.01, ** p<0.05, * p<0.1. All regressions control for income at entry, expected family contribution at entry, age, race, gender, SAT score, unemployment rate in home zip code, living on campus, and dependent status. They also include dummy variables for each year and institution fixed effects. | ||

The smaller coefficients for the higher EFC quartiles may be partly due to the fact that $1,000 constitutes a smaller portion of their total net costs. Thus, we reviewed the regression results using logged net costs to examine the effect associated with a 1% increase in net costs. These results are displayed in Table 5.3 and show similar patterns as the results in Table 5.2, although the effects of increasing net costs are now larger for the 3rd and 4th EFC quartiles. This makes sense given that a 1% increase in net costs is larger in magnitude for these students (with a 1% increase in net costs for the 4th quartile constituting $204, compared to $91 for the 1st quartile).[61] Once again, we find that net costs have a statistically significant and negative impact across the board on student success.

Table 5.3. Impact of a 1% Increase in Net Costs on First-Year Retention and Persistence

| First-Year Retention | First-Year Persistence | |

|---|---|---|

| 1% increase Net Cost | ||

| EFC Q1 | -0.03516*** | -0.02899*** |

| (0.00586) | (0.00432) | |

| EFC Q2 | -0.02136*** | -0.01727*** |

| (0.00531) | (0.00360) | |

| EFC Q3 | -0.05769*** | -0.03648*** |

| (0.00768) | (0.00524) | |

| EFC Q4 | -0.03737*** | -0.02057*** |

| (0.00648) | (0.00365) | |

| Clustered standard errors are in parentheses. *** p<0.01, ** p<0.05, * p<0.1. All regressions control for income at entry, expected family contribution at entry, age, race, gender, SAT score, unemployment rate in home zip code, living on campus, and dependent status. They also include dummy variables for each year and institution fixed effects. | ||

Other Measures of Student Success

We also looked at other indicators of first-year success and how net costs impact them. These results are presented in Table 5.4. We find that each additional $1,000 in net costs significantly reduces the number of credits earned in a student’s first year by 0.21 credit hours for students in the 1st EFC quartile. Some of this is due to these students attempting fewer credits, as a $1,000 increase in net costs reduces the number of credits attempted in year one by 0.051 credits. Thus, if we control for credits attempted in the credits earned model, we see that the effect on credits earned is reduced to -0.15 credits. Although these estimates are small, as we indicated above, the overall impact of rising net costs on an individual student’s chances of success are larger than that – students looking at rising costs are pushed to both take fewer credits and are less likely to complete the credits they do take.

Similarly, net costs reduce the rate of progress students make towards a four-year degree.[62] However, it is less clear what impact net costs have on the four-year graduation rate. The overall impact of net costs on the four-year graduation is statistically significant at the 95% confidence level when estimated across all students, and it is significant at the 99% confidence level within each EFC quartile. Although the effect is actually larger for the 2nd and 3rd quartiles than for the 1st and 4th, the effects across all quartiles are still relatively small.[63]

Table 5.4. Impact of $1,000 Increase in Net Costs on Additional Indicators of Student Success

| Credits Attempted Year 1 | Credits Earned Year 1 | Credits Earned Year 1, controlling for attempted credits | Progress Year 1 | Graduate in 4 years | |

|---|---|---|---|---|---|

| EFC Q1 | -0.05081*** | -0.20700*** | -0.14825*** | -0.00686*** | -0.00703*** |

| (0.01098) | (0.02148) | (0.01837) | (0.00071) | (0.00174) | |

| EFC Q2 | -0.05330*** | -0.17520*** | -0.11609*** | -0.00561*** | -0.00847*** |

| (0.00884) | (0.02129) | (0.01679) | (0.00069) | (0.00171) | |

| EFC Q3 | -0.05055*** | -0.10819*** | -0.05214*** | -0.00321*** | -0.01117*** |

| (0.00609) | (0.01598) | (0.01513) | (0.00055) | (0.00134) | |

| EFC Q4 | -0.04141*** | -0.07018*** | -0.02572* | -0.00202*** | -0.00579*** |

| (0.00683) | (0.01824) | (0.01472) | (0.00058) | (0.00115) | |

| Clustered standard errors are in parentheses. *** p<0.01, ** p<0.05, * p<0.1. All regressions control for income at entry, expected family contribution at entry, age, race, gender, SAT score, unemployment rate in home zip code, living on campus, and dependent status. They also include dummy variables for each year and institution fixed effects. | |||||

Thus, while all of our results find relatively small relationships to date between outcome indicators and net costs, these relationships are statistically significant at the 99% confidence level for all EFC quartiles in all but three cases, and are negative in all cases. The consistency of these results and the variety of outcomes we explored suggest that rising net costs do indeed have a statistically significant, negative effect on efforts to improve student outcomes. Consequently, if net costs continue to grow at rates similar to those Virginia has experienced since 2007, then we can only expect the sobering result that student success rates are very likely to decline.[64]

Supporting Evidence

While we control for student characteristics at entry and for institutional- and year-fixed effects in our OLS specifications, there may still be some unobservable student characteristics (such as intrinsic motivation) and institutional factors (such as policy changes) that affect these outcomes. While the large size and diversity of our population reduce some of the concerns about threats to internal validity, our confidence in these results is bolstered by their consistency across indicators and with previous research.[65] Nevertheless, we chose to conduct additional robustness checks on our original results in order to be as thorough as possible.

We examined the results from a hazard model to more precisely estimate the impact of net costs on each path that a student can take at the end of his/her first year. The results in Table 5.5 show how a $1,000 increase in net costs is related to the probability that a student follows a certain path at the end of year one (compared to the baseline path of remaining enrolled).[66] We see that all non-reenrollment paths are positively and significantly related to higher net costs, with a $1,000 increase in net costs associated with a student being 1.06 times as likely to not persist (by dropping out or taking time off).[67] Net costs do not have a statistically significant impact on whether or not students in the 1st EFC quartile transfer, although they do have a significant impact on the transfer patterns for students in the 2nd and 3rd EFC quartiles (with students in the 3rd EFC quartile being 1.04 times as likely to transfer given an increase in net costs of $1,000). These results also show that net costs are more related to persistence (rather than transfer) patterns for the separate EFC quartiles.

Table 5.5. Relative Risk Ratios of a $1,000 Increase in Net Costs on Not Persisting and Transferring, Compared to Remaining Enrolled after Year 1

| Not Persisting | Transferring | |

|---|---|---|

| EFC Q1 | 1.06172*** | 1.01988 |

| (0.00966) | (0.01276) | |

| EFC Q2 | 1.06146*** | 1.02337* |

| (0.01109) | (0.01226) | |

| EFC Q3 | 1.06121*** | 1.03902*** |

| (0.00939) | (0.00961) | |

| Clustered standard errors in parentheses and *** p<0.01, ** p<0.05, * p<0.1. All regressions control for income at entry, expected family contribution at entry, age, race, gender, SAT score, unemployment rate in home zip code, living on campus and dependent status. They also include dummy variables for each year and institution. Not persisting includes dropping out and/or taking time off. | ||